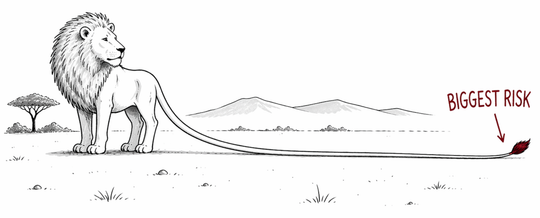

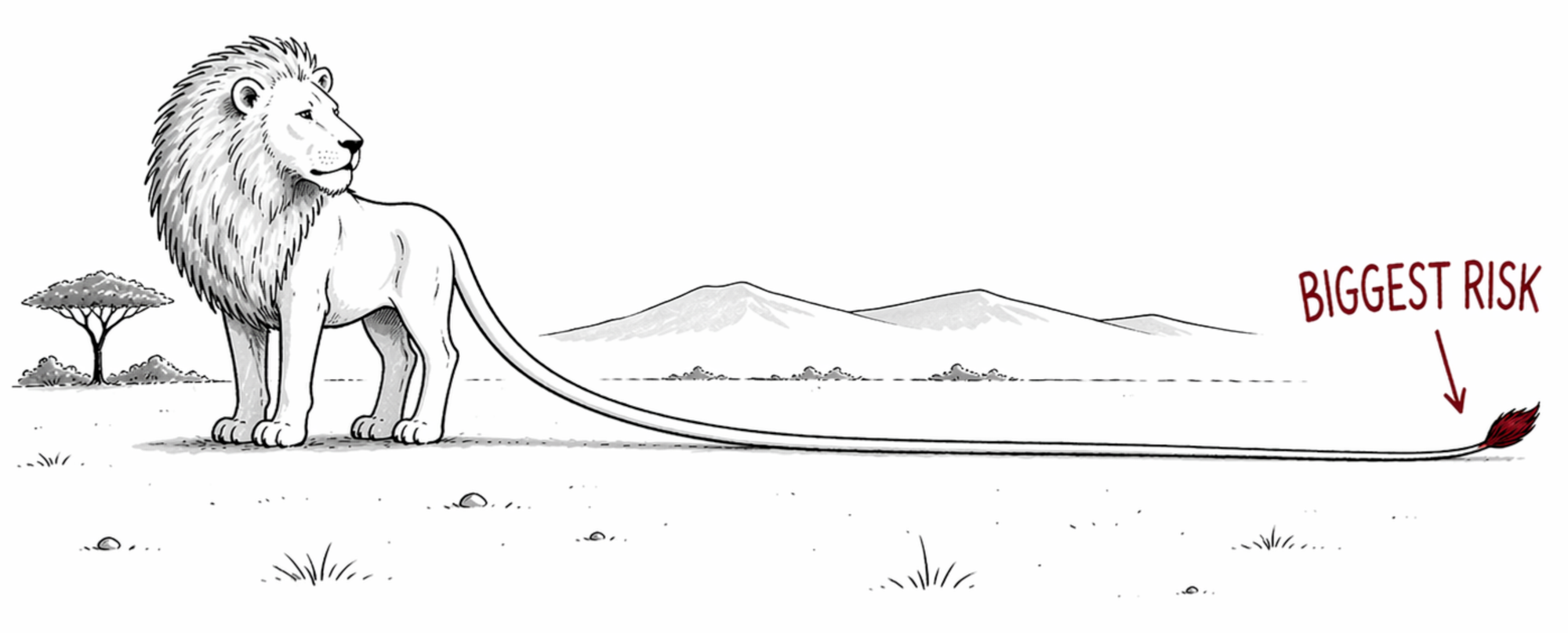

Many higher-net-worth clients can absorb an average long-term care event out of pocket, but don't want to pay for eight or more years of memory care costs. Below is one efficient approach to covering this long-tail risk.

What to know

- Elimination periods: State laws cap them at 365 days, limiting this deductible strategy.

- Alternative design: Shift more coverage to later years, where longer claims cost more.

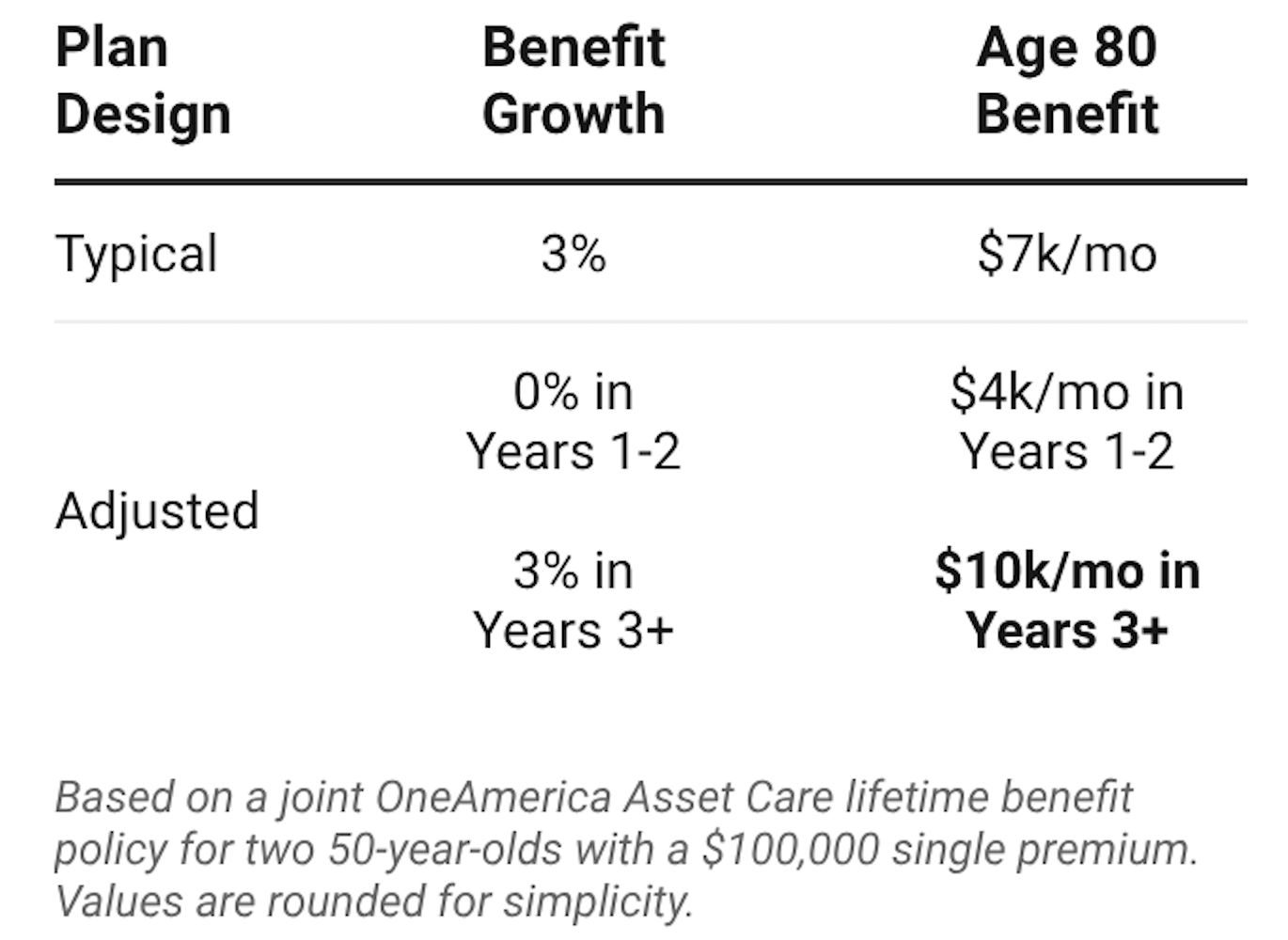

- Asset Care design: OneAmerica Asset Care, which offers lifetime benefits, can be structured with 0% growth on the first two benefit years, then 3% or 5% starting in year three, effectively moving more LTC coverage to later years.

In this example, adjusting the benefit growth shifts more care dollars to years three and beyond.

Planning implications

This design is well-suited for clients who aren't trying to insure everything. A short claim is manageable. A decade of memory care is not, and that's the scenario worth transferring.

The inflation structure reinforces this logic. Benefits are intentionally modest in the early years, then grow on the later years of a claim when total costs can get large. In my view, this is one of the more efficient uses of LTC premium for high-net-worth clients.

When to raise this with clients

- When a client has the liquidity to absorb an average LTC event of three years but wants protection against a prolonged claim

- When the client's primary concern is cognitive decline or a prolonged Alzheimer's diagnosis

Bottom line

For clients who can self-insure an average claim, a OneAmerica Asset Care plan design can offer lifetime coverage with back-loaded inflation, concentrating benefit growth in the later claim years when cumulative costs are highest.

Read a more detailed case study with specific quotes here.

Client resources: I publish short videos and articles explaining long-term care concepts for your clients.

Work together: I'm a long-term care specialist. In addition to articles like these, I help financial professionals evaluate coverage options for clients. Reply or schedule time to refer a client or discuss a case.

Best,

Jesse Vickey

Long Term What?

P.S. If this was forwarded to you, sign up to receive future emails.