Intro

Introduced in 2025, Nationwide CareMatters Annuity is an "annuity hybrid" (I'll explain this term in a bit) that pays long-term care benefits entirely as cash. That structure gives policyholders far more flexibility in how they use their benefits when it matters most.

In these policy reviews, I compare each to a pop-culture character. The other two CareMatters policies were matched with the Star Trek characters, Kirk and Spock, known for their bold, first-into-the-unknown leadership. So CareMatters Annuity feels like Jean-Luc Picard from Star Trek, who often lives in the shadow of these two stars, but he’s thoughtful, steady, and quietly effective. In certain situations, he’s exactly the right person to guide the ship.

Post jargon

annuity hybrid: a policy that combines an annuity with LTC benefits

benefit: the amount LTCi pays for covered care expenses

benefit period: the maximum time LTCi pays for care after criteria are met

benefit pool: total amount available in LTCi for care expenses

cash indemnity: pays the full benefit, regardless of the actual care costs

death benefit: a payout to a beneficiary from a hybrid policy after the insured passes away

elimination period: the waiting period after criteria are met before benefits start

inflation protection: LTCi benefit that adjusts for rising costs

life hybrid: a policy that combines life insurance with LTC benefits

non-qualified annuity: annuity funded with after-tax money; gains taxed on withdrawal

premium: the payment to maintain insurance

underwriting: insurer’s review process to decide coverage and cost

➡️ Explore all the LTC jargon

What is an annuity hybrid?

Most long-term care policies we review are life hybrids, combining life insurance with LTC benefits.

Bridge is different. It’s an annuity hybrid, meaning it pairs an annuity with LTC coverage instead of life insurance.

Common characteristics of annuity hybrids:

- Easier underwriting – More health conditions can be approved, often with just a short set of questions and no medical records.

- Tax-efficient transfers – Existing annuities can be moved via a 1035 exchange without triggering taxes. If used for LTC or paid to beneficiaries, gains are generally tax-free.

- Higher refunds – Compared to life hybrids, they often return more unused value to heirs.

- Appealing at older ages – These structures can be especially attractive for older applicants, particularly women.

Standard benefits

CareMatters Annuity comes with many standard benefits of a hybrid policy:

- Guaranteed benefits: Your payouts always match your policy terms.

- Benefit triggers: Coverage starts when you need help with two ADLs or cognitive decline.

- Broad coverage: Includes informal care (e.g., family), home health care, adult day care, assisted living, nursing homes, memory care, CCRCs, care coordination, respite care, and hospice.

- Inflation protection: Keeps your benefits aligned with rising costs.

- Death benefit: If you never use your benefits, your family receives a payout upon your death.

- Money-back option: Cancel your policy and get money back.

What's special about CareMatters Annuity?

In a competitive market, policies often include standout features to set themselves apart. Let’s take a closer look at what makes CareMatters Annuity special.

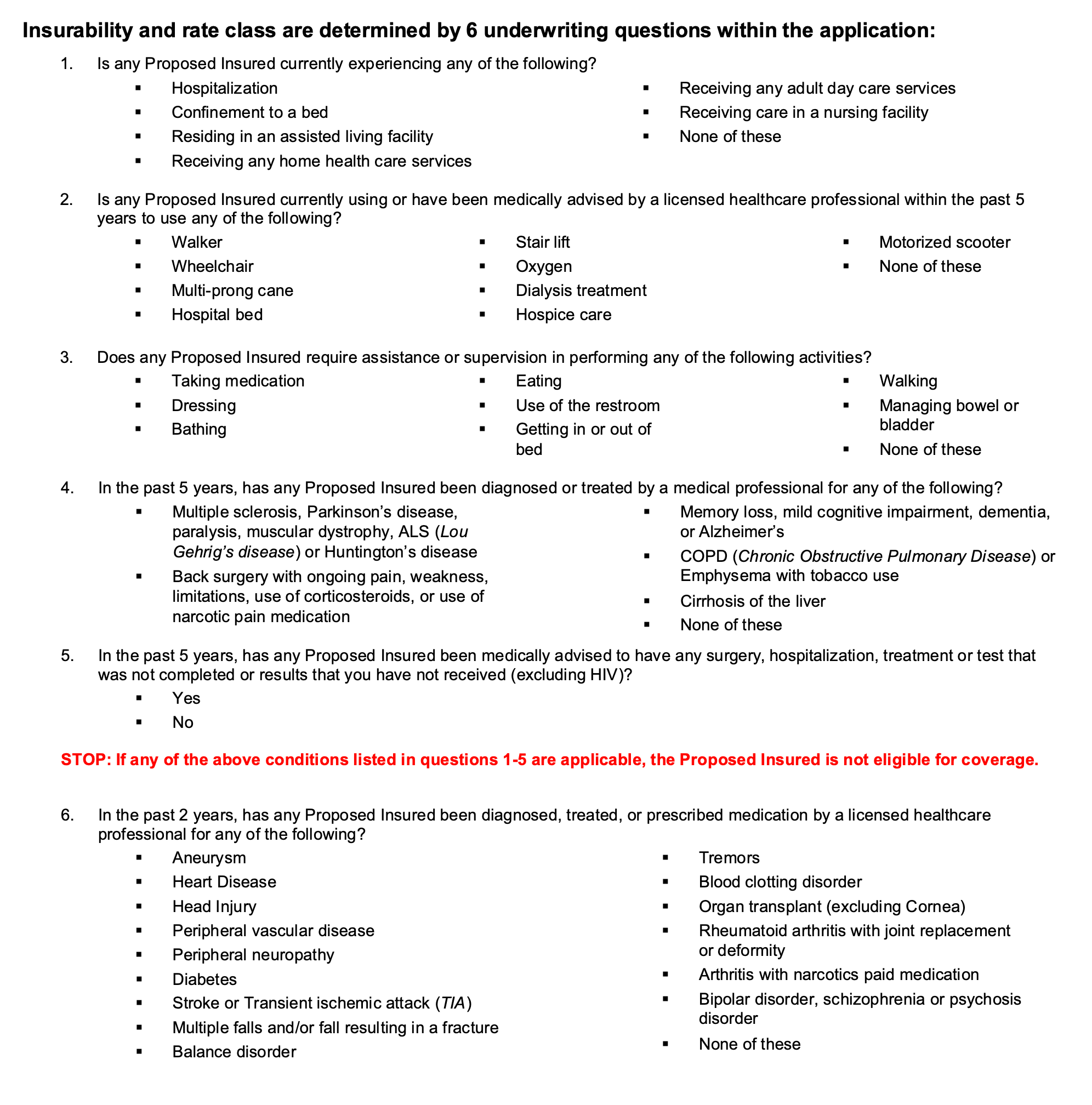

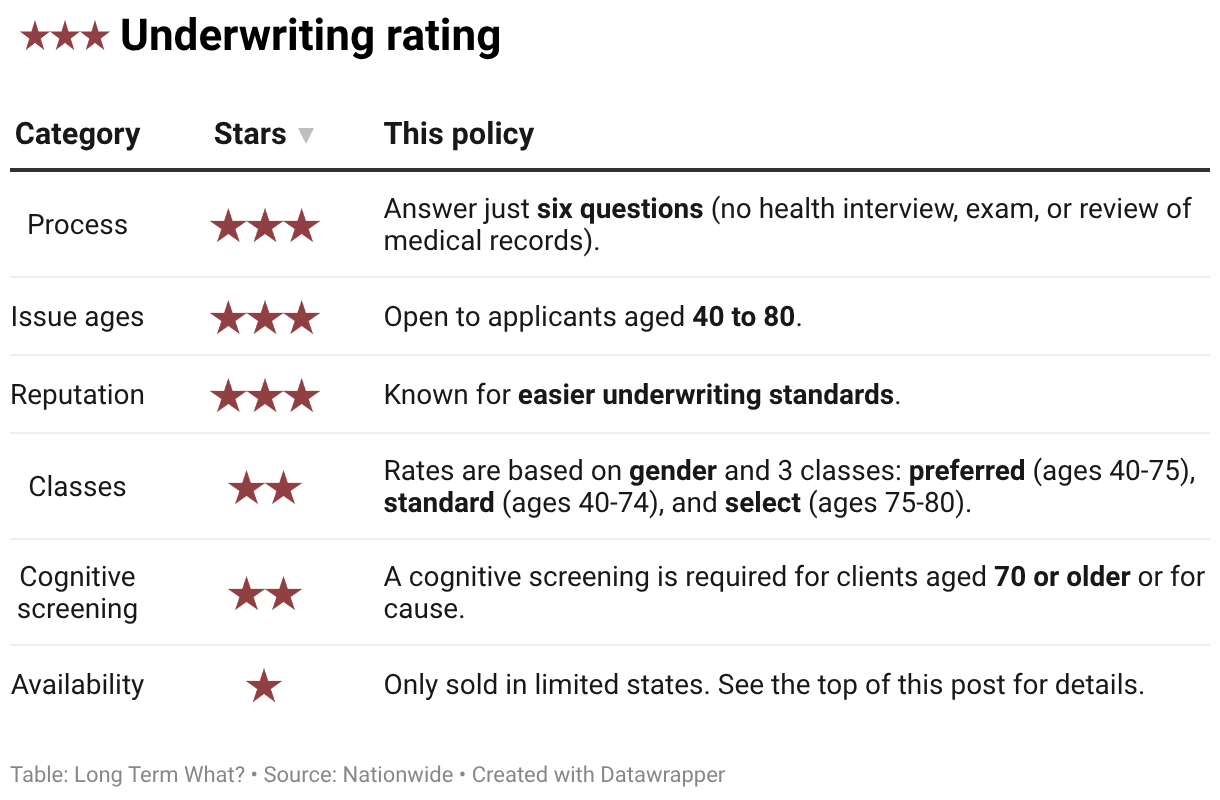

- Easier to qualify: Answer just six questions. There’s no health interview, exam, or medical records review, though prescription history is checked.

- Cash benefits: Pays cash (no receipts required), offering higher payouts and full flexibility on how you use the money.

- Guarantees: All rates are guaranteed for the life of your policy.

- Generous waiting period: Coverage starts after 90 days of needing care. You're then retroactively reimbursed for those expenses.

- High refunds (death benefit): Compared to life hybrid policies, refunds to your heirs are typically higher if you use little or no care.

- 100% international benefits: Get full LTC benefits if you're living abroad.

- Joint policy: Cover two people who share one pool of benefits paid over 9 years (instead of 6 years for individual policies).

How CareMatters Annuity works

Make a single up-front payment (for example, $100k). You cannot spread your payments over time.

Based on your health and age, your premium is doubled or tripled to pay for long-term care.

| Class | Issue ages | LTC benefits | LTC benefit period |

|---|---|---|---|

| Preferred | 40–74 | 3× | 6 years |

| Standard | 40–74 | 2× | 4 years |

| Select | 75–80 | 2× | 6 years |

For example, if you put $100k into the policy and qualify for the Preferred class, your LTC pool is $300k to pay for care.

Using this example, you have two buckets of money:

- Your money ("contract value", $100k): Grows at 3% or 5% per year guaranteed, reduced by policy charges. and pays for your care first.

- Total money ("total LTC benefit", $300k): Grows at roughly the same rate, and combines your money and their money into your LTC pool.

For example, for a policy with a six year benefit period, care is paid by your money for the first two years and their money for the last four years.

Your LTC benefits are paid out tax-free. If you never need care, your heirs generally receive the remaining value tax-free.

How underwriting works

Answer just six questions. There’s no health interview, exam, or medical records review, though prescription history is checked.

Nationwide has a few additional requirements, including height and weight guidelines, a cognitive screen for clients 70+, and a health pre-screen, but it’s more flexible than the life hybrid version of CareMatters.

The details

If this policy piques your interest, we’ll scour the galaxy for the key details and deliver only what truly matters.

We rate each policy’s benefits, premiums, underwriting, and company on a three-star scale, with three stars being the best.

Benefits

Benefits are what the policy pays for covered care expenses.

CareMatters Annuity combines key hybrid policy benefits: cash indemnity, minimal exclusions, a death benefit, plus a strong benefit pool.

Premium

Premiums are the payments made to maintain insurance coverage.

Underwriting

Underwriting is how an insurance company evaluates your health and history to determine coverage and pricing.

CareMatters is widely available with a streamlined underwriting process, providing quick decisions.

Company

Choose a top-rated insurer for reliable LTC coverage, even decades from now. We only offer policies from financially strong companies to give you peace of mind.

Nationwide's experience and ratings are average compared to the policies we offer.

Comparisons

How does this policy stack up against others? Focus on what matters most to you to find the best fit.

In this table, you can compare the benefits of all the LTCi policies we offer. You can:

- Search for any detail.

- Tap any column title to sort.

- Scroll right to view more columns. ➡️

Next steps

If this policy seems like a good fit, click the button below and include 'CareMatters Annuity' in the notes section at the final step.

Wrap up

In the universe of long-term care insurance, CareMatters Annuity is the Jean-Luc Picard of the lineup. It is not the flagship option like CareMatters or CareMatters Together, but it is still confident, flexible, and quietly effective. In the right situation, it can be the better choice.

This policy is ideal if you’re looking for:

- Flexibility – thanks to cash indemnity benefits

- Tax benefits - when moving funds from an annuity

- High refunds – from a prioritization of your cash growth

- Peace of mind – from a trusted name in insurance

Also compare this policy to to EquiTrust Bridge:

| Feature | CareMatters Annuity | Bridge |

|---|---|---|

| Leverage if 75+ | 2x max | ~3x |

| Growth (your money) | 3% guaranteed | Not guaranteed, more upside |

| Underwriting | Stricter | Easier |

| Access | Full benefits at claim | "Their money" vests 20%/yr |

| AM Best rating | A+ | B++ |

If it sounds like a good fit, we're here to help you explore the details.