📺 Watch this and other posts on YouTube or listen on Spotify, Apple Podcasts, and YouTube Music.

Intro

Experts often recommend buying long-term care insurance (LTCi) in your 50s. That’s not bad advice, but we believe earlier is better—no matter your age, for three reasons.

Among these three, the biggest reason is to avoid The Thing so you pass underwriting. So, what is The Thing?

- Is it that superhero with orange, rock-like skin who can lift over a hundred tons? No, not this time. But you’d probably want to steer clear of him anyway, particularly when choosing a partner for synchronized swimming.

- In this context, The Thing is the health issue that sneaks up on you and makes you ineligible for coverage. It happens more than you would think.

If you've ever wondered, "Yeah, The Thing is strong. But can he build a kiddie slide?" Check out this 10-second clip.

Remember to use the letters LTC as a guide to achieve these goals: Learn about options, Talk with family, and Create a plan. Figuring out if and when to buy LTCi is a big part of securing peace of mind for the future.

Post jargon

Alzheimer's: the most common type of dementia (memory impairment or loss)

dementia: a broad term for memory issues, including Alzheimer's

LTC: long-term care

LTCi: long-term care insurance

underwriting: insurer’s review process to decide coverage and cost

➡️ Explore all the LTC jargon

The reasons to buy early

Why buy long-term care insurance (LTCi) early? Here are three key reasons that show why acting sooner can make all the difference. Let’s dive in.

Reason 1 - Pass underwriting

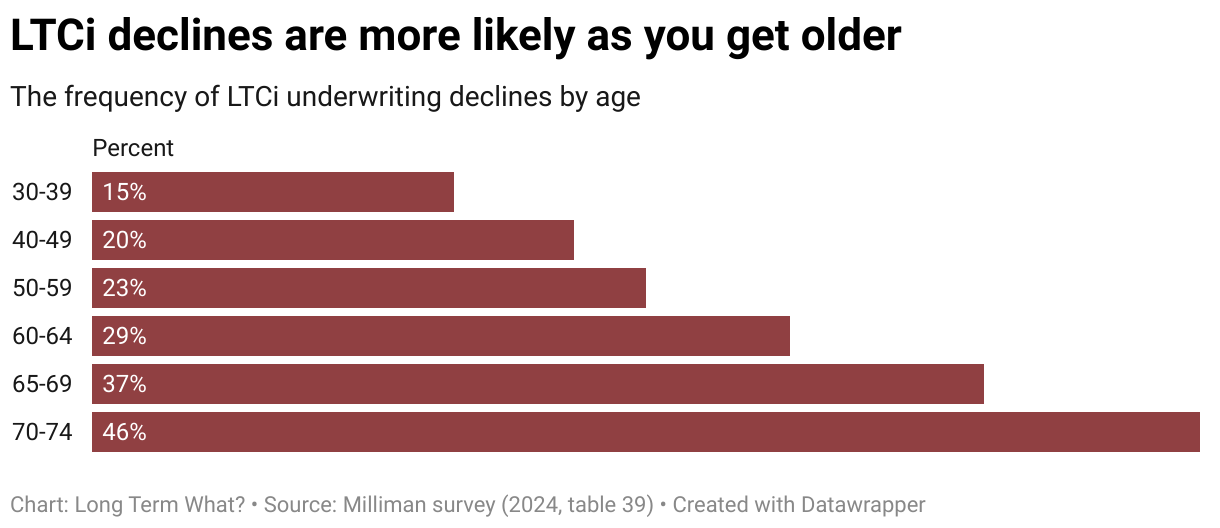

The first and top reason to buy LTCi early? Avoid The Thing—a health issue that pops up that could severely limit your options or disqualify you from coverage altogether.

When you apply, insurers undergo an underwriting process, where they turn into health detectives. They're looking for reasons to deny you coverage or charge you more for it. For those over 65, this can even include memory tests, like recalling words over the phone, as part of the cognitive assessment.

What counts as The Thing? It could be:

- A diagnosis like cancer, Parkinson’s, MS — or diabetes with complications

- Joint or back issues that led to steroid shots or physical therapy

- Memory trouble flagged during a screening or doctor visit

- Your parent was diagnosed with early-onset Alzheimer’s

- A recent surgery — or one that’s still being planned

Unexpected health issues are more common than you might expect, as shown by the increasing number of people who are declined coverage as they age.

But passing underwriting isn’t the only reason to act early. Let’s dive into another key reason: getting coverage now.

Reason 2 - Get early coverage

With home or auto insurance, you buy coverage ONE YEAR at a time. But with LTC insurance, you get coverage whenever you need it—whether that’s now or decades down the road—for as long as your policy allows.

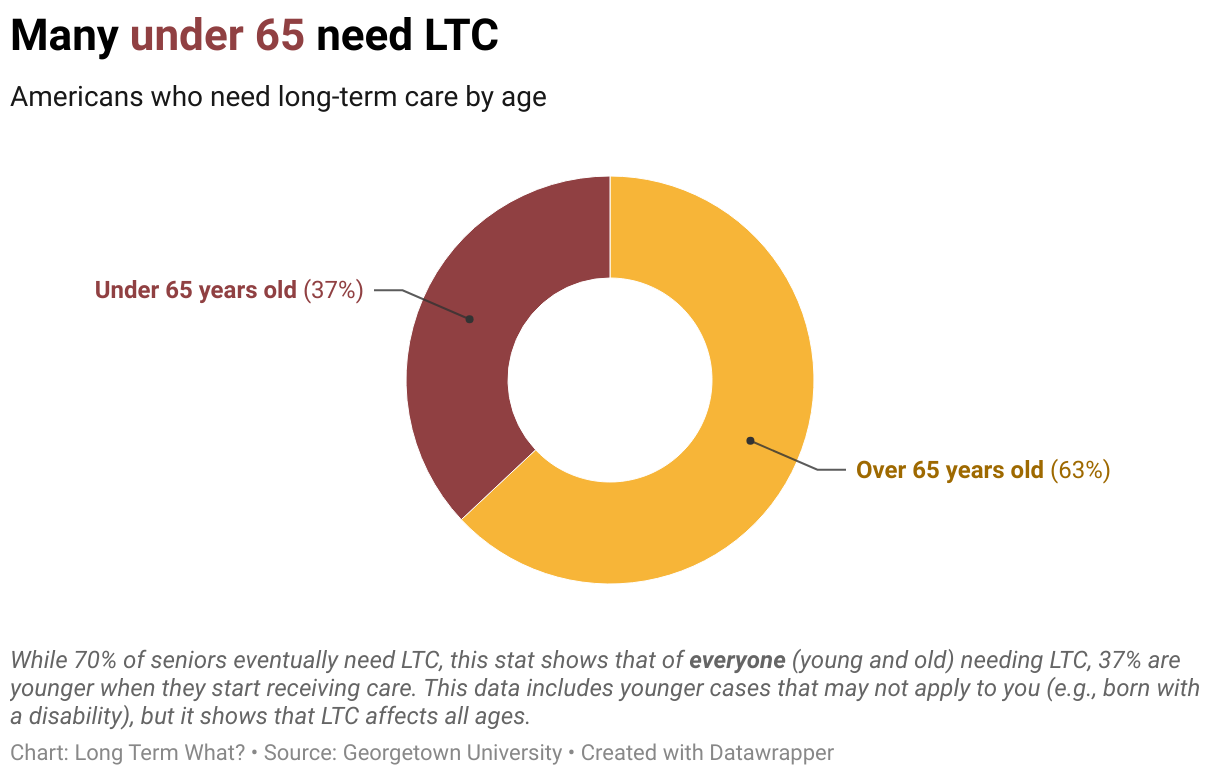

By buying early, you're protected if The Thing happens unexpectedly. Many people need long-term care before they're 65.

It's possible. A study conducted by Georgetown University in 2000 showed that 37% of those receiving long-term care were under 65, often due to chronic conditions, injuries, or disabilities. 👀

Buying early means you'll have coverage from day one. But at what cost?

Reason 3 - Save money

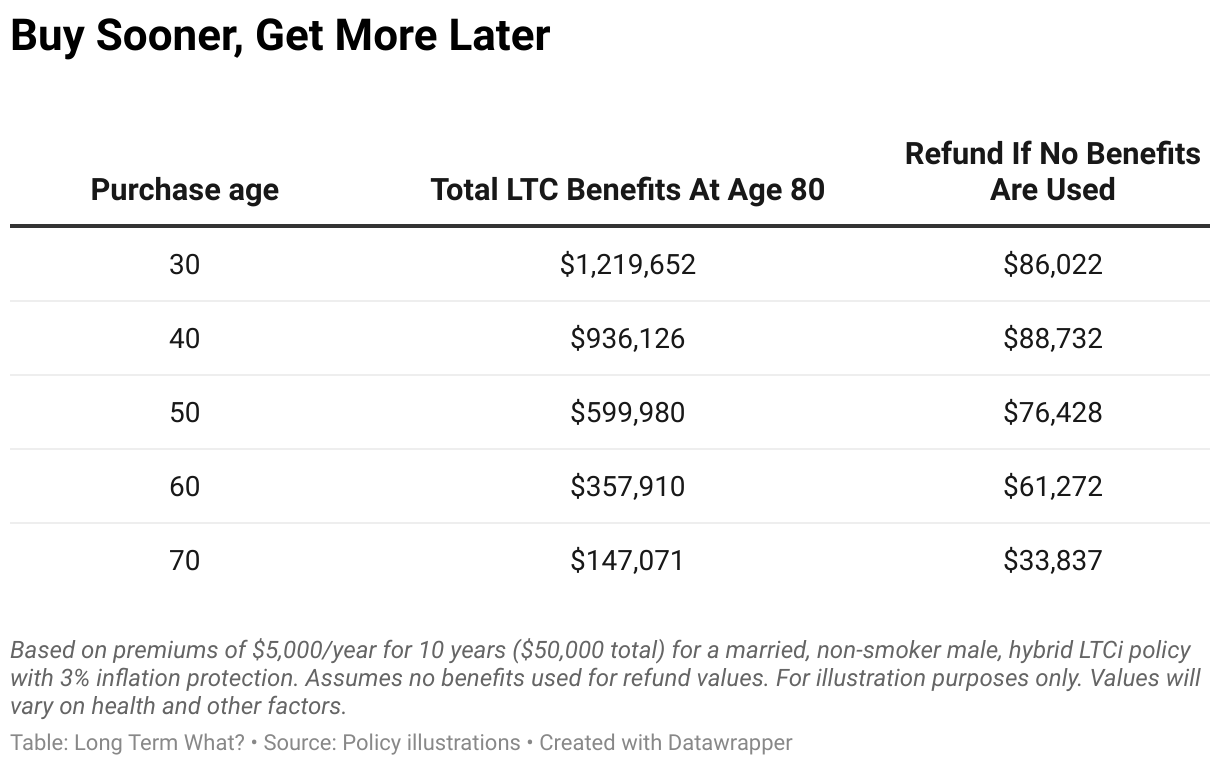

You might assume early coverage costs more since you'll have it longer, but the opposite is true.

The total cost of long-term care insurance is cheaper the younger you are. Here’s why:

- More time - Insurers expect you won’t need the coverage for a while, so they can earn interest on your premiums for longer.

- Healthier - You’re likely healthier now than later, which means lower rates (better health class).

Let’s compare the benefits of buying a popular LTCi policy—$5,000/year for 10 years ($50,000 total)—when starting at different ages.

Or you can wait

But of course, not everyone does or can buy early. Here are some reasons why waiting might make sense for you.

- Higher priorities – Maybe you’re saving for your kids’ college or something else more important. Our take: We agree.

- Self-fund – You could invest your savings and plan to cover care costs out of pocket. Our take: Maybe. Check out our post on self-funding.

- Wait for a better fix - Hope that Medicare, AI, or something else solves long-term care. Our take: It’s a long shot.

Buying LTCi by age

As you consider long-term care insurance, your age plays a big role in cost, eligibility, and plan options. Here’s what to keep in mind at each stage of life.

In your 30s

You’re likely focused on your career or building a family. With time, good health, and the lowest rates on your side, it’s one of the best times to buy LTCi—if you can afford it. While a few insurers don’t offer coverage this early, it’s a rare chance to lock in the best pricing while you're at your healthiest. Buying in your 30s is like grabbing first-class tickets at economy prices—it won’t get cheaper later.

In your 40s

You may be juggling kids, career, and mortgage payments. Your health is still strong, and premiums remain very reasonable. All insurers offer coverage at this age. If you can afford annual payments, your 40s are a smart time to lock in coverage at favorable rates.

In your 50s

Your kids may be heading off to college, and your retirement savings are growing. This is when most people buy coverage—the average buyer is around 55. You’ve likely seen friends or parents need care, so the value of LTCi feels more real. Rates are a bit higher than in your 40s but still reasonable. This is the 'get it done before it gets harder' decade.

In your 60s

Retirement is on the horizon, and health issues may start to surface. Many people buy coverage in their 60s, but insurers begin screening for signs of cognitive decline—often using phone-based memory tests. Approval rates drop as more applicants are declined for health reasons. If you haven’t purchased coverage yet, now’s the time—getting approved becomes much harder in your 70s.

In your 70s

You may face more health issues, and the need for care feels closer. This is the final window for most people to apply—insurers typically stop offering coverage after age 80, and some stop even earlier. Decline rates are high, and premiums are steep. But if you’re healthy, this is your last real chance to get meaningful coverage.

Wrap up

In the end, deciding when to buy LTCi depends on your personal situation. Luckily, you’ve got a wide age window—policies are available for those who are 30 to 80 years of age; most people buy at around age 57.

But remember, waiting too long risks encountering The Thing—not the superhero, but that sneaky health issue that can block your coverage. Just like you wouldn’t want The Thing weighing you down in the pool, you don’t want health surprises to sink your chances of getting the coverage you need.

If insurance is part of your plan, buying early is often your best bet. It gives you a better chance at locking in lower rates and more coverage—before anything unexpected shows up.