Carol and Laura,

Good news. Your revised long-term care (LTC) insurance quotes are ready.

🔁 Revised quotes

I’ve provided three quotes, each with $6,000/month in benefits starting on day one so you can compare them directly. Each option includes 3% annual growth to help the benefits keep pace with rising long-term care costs. These are all quoted as a single premium, but below the table are longer payment options with smaller premiums, all guaranteed never to increase.

💰 Payment options

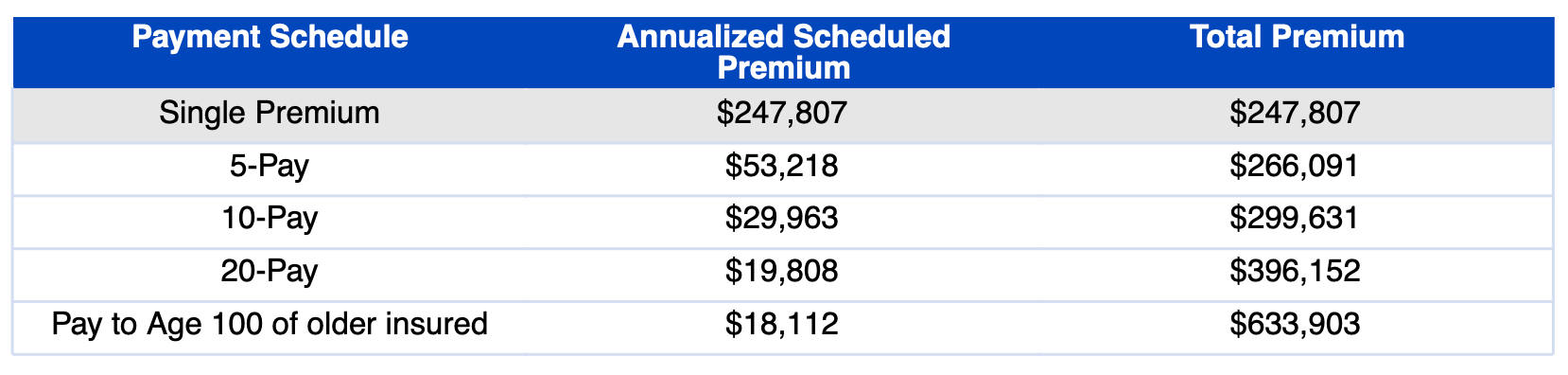

Each policy includes multiple payment options. The figures below are annual premiums. Monthly payments are available and cost slightly more than 1/12 of the annual amount.

Option A: Nationwide CareMatters Together

Both the 20-pay and pay-to-age-100 options are under $2,000/month.

Option B: Lincoln MoneyGuard

These two individual policies are slightly less than the Option A grid above, but it offers 5-year and 10-year payment schedules only. If you prefer a longer payment period, we could also look at similar individual policies with 20-pay options.

Option C: OneAmerica Asset Care

The pay-to-age-95 option is roughly $2,000/month.

🧐 My notes

All three options are strong and each includes a refund to your heirs if you never need care.

Option A: This joint policy from Nationwide CareMatters Together lets you share a total benefit pool equal to 8 years of care. For example, one of you could use 2 years and the other 6 years, or one person could use all 8 years. For shorter benefit periods, this is often one of the most cost-effective choices for couples.

Option B: This includes two individual policies from Lincoln Financial. Each of you would have 6 years of benefits, and the total premium is lower than Option A. Neither of you could access 8 years individually like Option A, but the combined total benefit pool is higher. Benefits are paid as reimbursement or 80% in cash.

Option C: This joint policy from OneAmerica offers lifetime benefits, the gold-standard. It costs more than Options A and B and has a smaller refund if care is never needed. Benefits are mostly reimbursement, with 75% available in cash for the first two years. But it provides extended coverage for both of you in the case of Alzheimer’s or other memory care needs.

My thoughts: I'd go with option B for the lowest cost or option C for the longest benefits.

Assisted-living in New Jersey is projected to cost $185k/year by age 80 (assuming 4% annual growth). Your options provide lower annual benefits than this projection ($112k/year), but you can bridge the gap using personal savings and Social Security. The goal for most people is meaningful coverage, not paying every dollar.

If you'd like to adjust your annual benefits, you can adjust your premium—your benefits will change proportionally (e.g., by 25%).

👉🏻 Next steps

If any of these policies look appealing, please schedule time on my calendar so we can review the options together and address any questions you may have.

If you want to skip a call for now, I recommend both of you completing this longer health pre-screen form (15 minutes). I’ll share your answers anonymously with insurers to get informal feedback before any formal application. This helps us identify which policy is the best fit and avoids the risk of a formal decline.

Once I receive the feedback, we can schedule a call to review your best options together. 👍🏻

📺 Still learning?

Watch our "unboring" video on qualifying for LTC insurance or visit our website. That's me in the video.

Thanks,

Jesse

Jesse Vickey at Long Term What?

Schedule a call or 720-263-2188