📺 Watch this and other posts on YouTube or listen on Spotify, Apple Podcasts, and YouTube Music.

Intro

Do you remember the dating scene in 4th grade? It was super awkward.

If you liked someone, you’d scribble a “Do you like me?” note, hand it to a friend, who’d sneak it over to your crush.

Then it came back with a brand-new option checked off. 😔

Qualifying for long-term care insurance is a lot like 4th grade dating. It’s awkward, full of note-passing, and the answers aren’t always just yes or no. Read on and I'll show you what I mean.

Post jargon

benefit: the amount LTCi pays for covered care expenses

claim: a request for benefits when LTC is needed

LTC: long-term care

LTCi: long-term care insurance

NAIC: National Association of Insurance Commissioners; sets standards for state insurance regulation

preexisting condition: an illness treated before applying for LTCi

premium: the payment to maintain insurance

➡️ Explore all the LTC jargon

The basics

You’re not guaranteed to get long-term care insurance the way you might with other health plans. Your current health and health history play a big role in whether you qualify and how much you’ll pay.

There are about ten top-tier insurers offering competitive pricing. These insurers all employ smart nerds to decide who to accept and what to charge.

After looking through decades of data, each insurer makes its own bets on who’s likely to need care … decades from now. Each insurer looks at age, gender, and health a little differently. Some are stricter about diabetes, cancer history, or weight.

If you have health concerns, checking with multiple insurers really matters. It may be easier to get a yes from one company than another.

With that in mind, today I’ll guide you through a process called underwriting. It’s basically the dating stage between you and insurers where they size you up.

Age

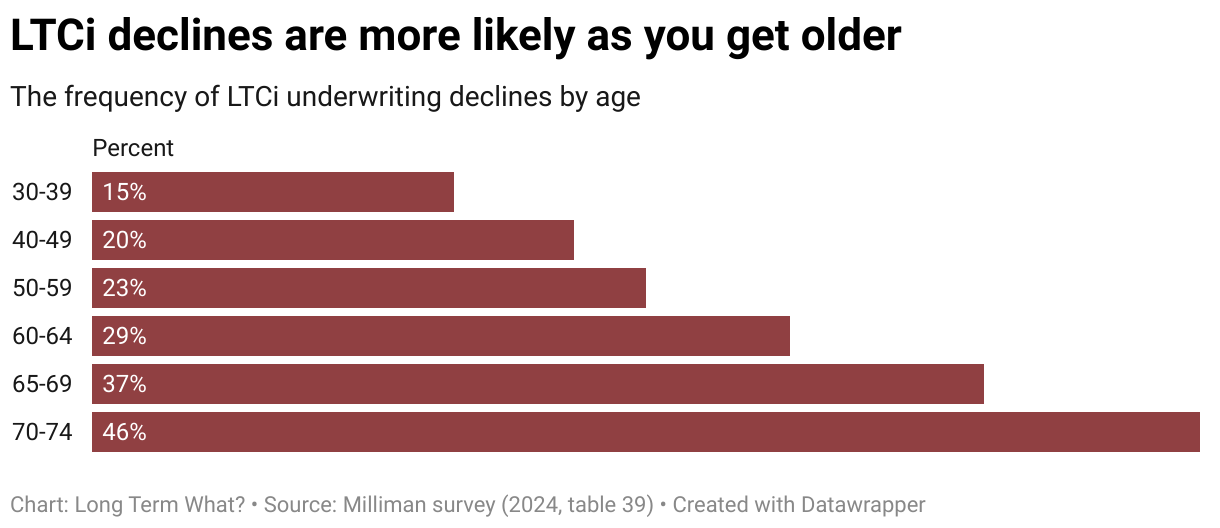

Age plays a big role in underwriting. Some insurers won’t offer coverage if you’re younger than 40 or older than 75. And the older you get, the tougher it becomes to qualify.

The numbers tell the story: in your 30s, only about 15% of applications are declined. By your 70s, almost half get a no.

That’s why it pays to apply earlier rather than later. We cover the best age to buy long-term care insurance in another post.

Pre-qualification

Getting pre-qualified by an insurer is really important, and most people have no idea it even exists.

Remember in 4th grade when you passed that “Do you like me?” note? You passed a note because you didn’t want the whole class to hear the answer. Shopping for long-term care insurance works the same way. You want quiet feedback before an official decision gets shared with other insurers.

That’s why we offer pre-qualification. This is different than a formal decision which gets logged in the Medical Information Bureau, or the MIB. And no, not that MIB with Will Smith.

This one’s waaay less fun. It’s a database where insurers share findings and check before deciding whether to approve you. If one company says no, other insurers can see the no, which can make approval elsewhere much harder.

Pre-qualification avoids all that. You fill out a thorough health intake form, and we anonymously share it with a few insurers—no name attached.

They quietly respond with a green light, red light, or "let’s wait". If you’ve had a recent procedure, are doing physical therapy, or have a pending test, they might ask you to wait a few months before applying.

Insurers like the pre-qualification process. It saves them from pulling full medical records on cases that aren’t a fit.

Pre-qualification isn’t a guarantee, but it gives you the best path forward before you make anything official.

Application

Once you’ve received the green light on your pre-qualification, it’s time to formally apply.

Each insurer handles the application process a little differently. Some let you submit everything online, while others require a phone call. Which feels a bit dated (sigh).

Either way, you can expect plenty of questions, just like the ones you answered in your pre-qualification.

- Have you had any surgeries in the past 10 years?

- Are you taking any prescriptions?

- Any cancer history?

- Any scheduled treatments?

Have your answers ready to help the call go smoothly.

How do they check?

This varies by the applicant and insurer.

- If you have some health issues, you may be asked to draw blood.

- If you’re over 65, many insurers require a phone or online cognitive test. You might be asked to recall words or answer basic questions. Sometimes, a nurse may visit your home to check your ability to live independently.

After they get information from you, insurers usually review your prescription history from another database and may also request medical records from your doctors.

The process can take anywhere from a few days to two months, depending on the insurer and your health.

What do they check?

They’re on the lookout for high risks that suggest you might need long-term care for an extended period. Or, if you choose a policy that combines life insurance, that you might pass away prematurely.

If you currently need long-term care due to Alzheimer’s or need help with activities of daily living—like bathing or dressing yourself—you likely won’t be eligible. Other examples of knockout issues include Parkinson’s, MS, current cancer, or a stroke with lasting impairments.

With that said, human bodies are complicated, full of grey areas. Some people can shoot webs from their wrists.

That’s why insurers often look at multiple factors. One condition—like diabetes—might be acceptable, but two related conditions—like diabetes and a high BMI—can raise concerns.

Rate classes

If you're approved, you'll usually be placed in a rate class—like Preferred or Standard—based on your level of risk. Sometimes smoking gets its own rate class. Landing in the Preferred class means you’ll pay less than people in a lower class.

Approval

Then it’s time to celebrate… you’re approved. 🎉

The good news is once you’re approved, you’re covered for everything in your health history—no fine print about pre-existing conditions.

Your policy can kick in anytime down the road and lasts for 3 years, 8 years, or however long you bought it for.

Your policy cannot be canceled as long as premiums are paid.

- In first two years, if you file a claim, your insurer has the right to review your application to confirm the information you provided was accurate.

- After two years, the policy generally becomes incontestable for honest mistakes or omissions.

However, intentional misrepresentation or insurance fraud, such as falsifying documents, can allow the insurer to deny a claim at any time.

All of this gives you real peace of mind as you get older.

Wrap up

Qualifying for long-term care insurance is a little like 4th grade dating. We’re still passing notes, hoping for that big yes, and doing everything we can to avoid the dreaded “as a friend” checkbox.

If you work with Long Term What? to get coverage, our job is to quietly pass your note to insurers to find the best fit for approval at the best rates.