📺 Watch this and other posts on YouTube or listen on Spotify, Apple Podcasts, and YouTube Music.

Intro

I purchased my first care in high school. It was a used 1986 Toyota Celica GTS in faded red that included a sunroof and a tape deck. I was cool.

All cars get you from point A to point B—but the features make a big difference. Now that I have a family in Colorado, where it snows, a blue CrossTrek with four doors and all wheel drive is cool. 😎

All long-term care insurance policies pay for care—but the features make a big difference. As you plan for your older self, you’ll want a set of features designed for you that make you cool. These might include:

- Reimbursement

- Cash indemnity

- Inflation protection

- Death benefit

- Payment schedules

- Elimination periods

- Benefit period

- Tax benefits

Looking ahead to features you want is smart planning. Remember to use the letters LTC as a guide to achieve these goals: Learn about options, Talk with family, and Create a plan.

This website is here to explain your benefit options in plain English, so you can make confident, informed choices when selecting a policy.

Post jargon

ADLs (activities of daily living): basic tasks like bathing, dressing, eating, transferring, toileting, and continence

benefit: the amount LTCi pays for covered care expenses

exclusion: an insurance rule that denies benefits for specific risks

LTC: long-term care

LTCi: long-term care insurance

➡️ Explore all the LTC jargon

Reimbursement

When you need long-term care, you'll get paid from your LTC insurance policy. Many traditional and older hybrid policies offer reimbursement. You submit receipts to your insurer for your care, and you're reimbursed for the costs.

Lower payments

Let’s say your maximum monthly benefit is $5k, but your LTC costs are $2k. You only get reimbursed for the $2k. You don't get the full $5k.

The problem of lower payments is worth repeating. Tune in.

| If your max benefit is | And your cost is | Then you get |

|---|---|---|

| $5k | $2k | $2k |

This might seem fair, but cash indemnity policies (which we’ll cover in a minute) pay you the full $5k.

More exclusions

Check your reimbursement policy's exclusions (i.e., reasons you won’t get paid). Some of these are pretty important.

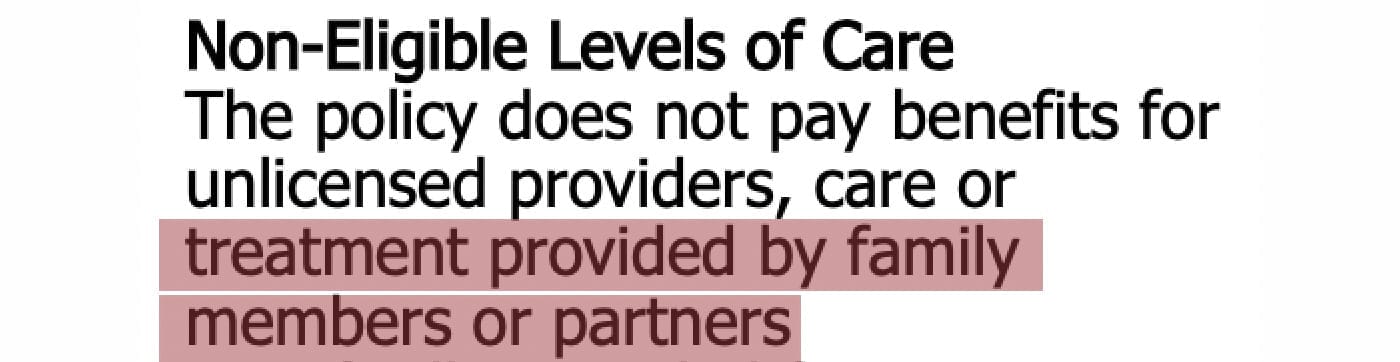

- Excluded: Unlicensed caregivers

Many reimbursement policies won’t cover care provided by your adult child, spouse, or other non-licensed caregivers. This limitation can seriously reduce your flexibility.

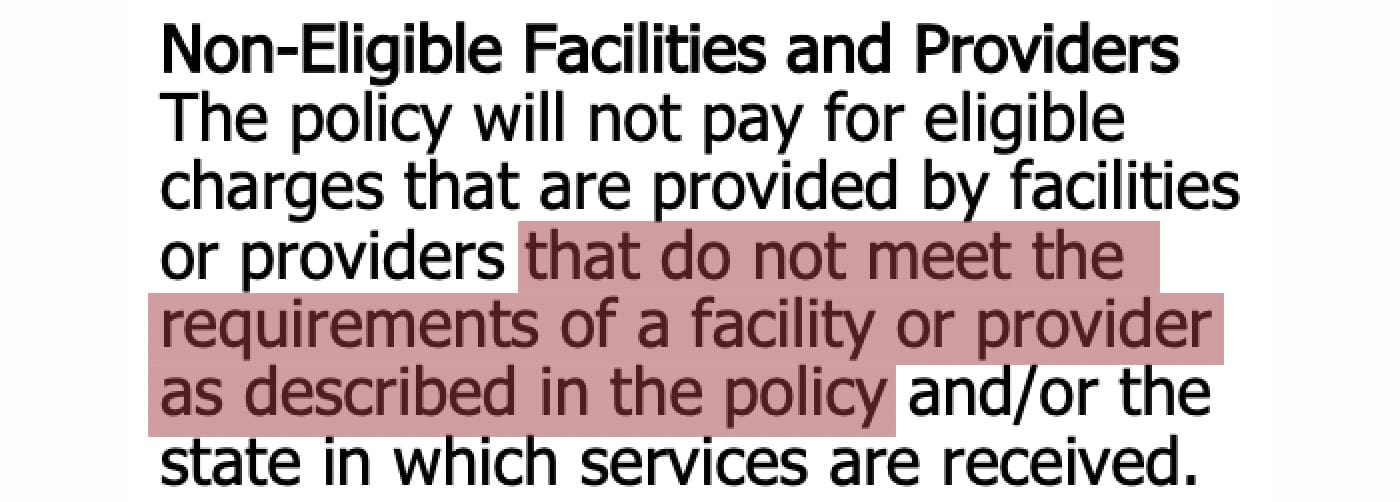

- Excluded: New types of care

Many reimbursement policies won’t pay for new types of care (👋 hello, AI?). They stick to eligible facilities or current standards of care. Who knows what the world will look like in 20 years? Unfortunately, your policy might not keep up.

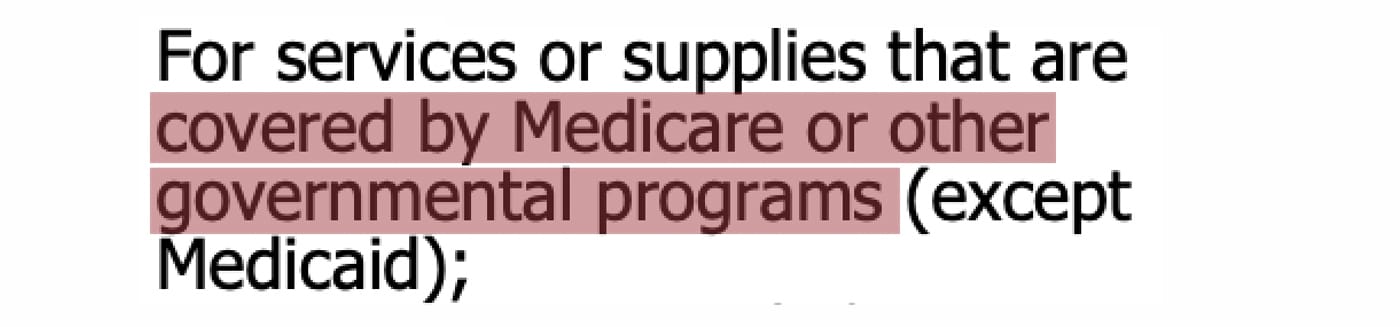

- Excluded: If Medicare pays

Many reimbursement policies won’t pay if another source, like Medicare, covers your care. While Medicare doesn’t currently cover long-term care (LTC), what if it starts covering parts of it in the future? It’s unlikely—but you’re buying insurance to reduce risk, so don’t take chances.

Cash indemnity

When you need long-term care, you'll get paid from your LTC insurance policy. Policies with cash indemnity are a big improvement compared to reimbursement plans.

But first, let’s talk about the term "cash indemnity." The insurance industry desperately needs a naming consultant.

Quick digression: My daughter showed me her pre-workout supplement called "Gorilla Mode: Tiger's Blood."

Now that's a catchy name. If the insurance industry sold this product, they’d call it "Betaine and Hydroprime Glycerol Powder." But whatever.

How cash indemnity works

Cash indemnity might sound boring, but it offers more money and flexibility with fewer hassles. Modern hybrid policies use this payment method, which has several perks:

- No need to submit receipts (less hassle).

- You receive the full, maximum benefit each month, regardless of the actual cost of care.

- You can spend the money on any type of care—no restrictions or approvals needed with fewer exclusions.

These improvements are a game changer. Let's dig into each one.

No receipts

Cash indemnity allows you to skip the hassle of submitting receipts, giving you more flexibility in how you use your benefits. However, many larger care providers, such as home care agencies, often handle reimbursements directly with your LTC insurance, ensuring they are paid without extra effort on your part.

Higher payments

If your monthly benefit is $5k and your care costs $2k, you still receive the full $5k (unlike reimbursement policies, which will only pay $2k).

| If your max benefit is | And your cost is | Then you get |

|---|---|---|

| $5k | $2k | $5k |

With cash indemnity, you pocket an extra $3k ($5k minus $2k) for anything you want—like a trip to see your grandma.

Fewer exclusions

Since cash indemnity policies don’t reimburse for specific services, there are far fewer exclusions than reimbursement policies. This flexibility allows you to pay for family caregivers or any expenses you choose.

Cash indemnity payouts typically have only a few exclusions:

- intentional self-harm

- felony involvement

Put another way, if and when we receive care from AI robots, you'll still receive benefits with cash indemnity policies.

Other considerations

Cash indemnity policies offer more flexibility than reimbursement policies. However, they typically cost a little more, and exact comparisons can be tricky due to policy differences.

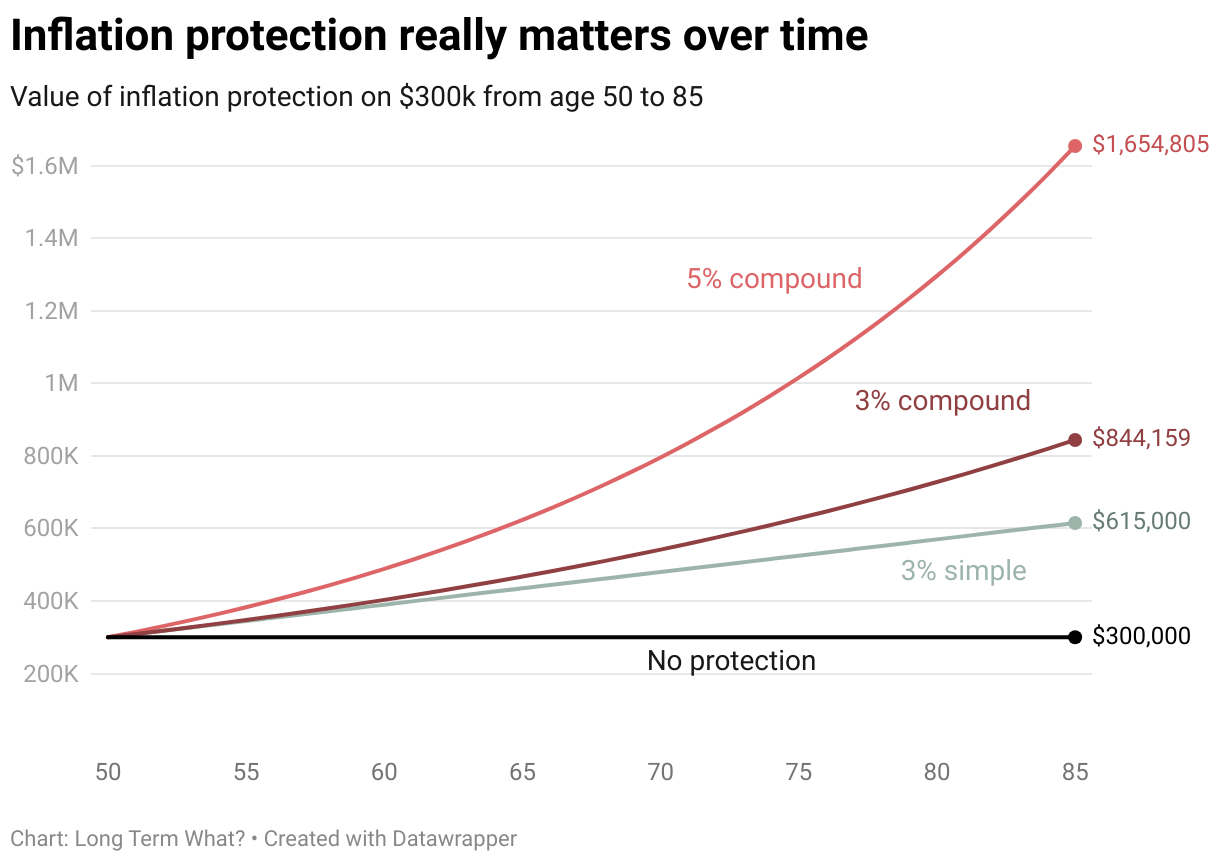

Inflation protection

Long-term care costs have risen 4% per year over the last two decades. You’ll want your policy to keep up with the rising cost of care.

Most LTCi policies offer two main types of inflation protection:

- Simple inflation protection: Your benefit increases each year by a fixed percentage based on the original amount. 👍🏼

- Compound inflation protection: Your benefit increases each year by a percentage of the previous year’s amount, creating a snowball effect—essentially interest on interest. 👍🏼👍🏼

As expected, compound inflation protection grows your benefits faster over time.

Bigger benefits come at a higher cost in premiums, but 3% compound inflation protection is the most common choice.

Some policies offer other types of inflation protection:

- 3% compound for 20 years - After 20 years, your benefits stop increasing. This can be a good choice if you're older and don’t expect to need coverage beyond 20 years.

- Compound on an index - Your benefits grow based on the actual rate of LTC inflation or a stock market index.

Death benefit

The term "death benefit" sounds weird and insensitive. You pass away, and someone gets paid?

But it’s practical. During a difficult time for your family, your family or beneficiary receive a tax-free payout when you pass away.

- For example, $100k in premiums could leave $150k for them.

- If you use some benefits while alive, that amount is subtracted from the payout.

Death benefits with traditional policies

Most traditional policies don't include death benefits. However, some offer a "return of premium" rider as an optional add-on, which functions similarly.

Death benefits with hybrid policies

Death benefits are standard with most hybrid policies. Even if you use your LTC benefits, hybrids typically guarantee a minimum death benefit—often around $10k—to cover final expenses like burial costs.

Payment schedules

Most insurers give you a few ways to pay—once, over 10 years, or even longer. After you’ve finished paying, you’re done for good and your benefits can kick in at any point down the road.

Cute little puppies

OK, we’ve been covering a lot. Let’s take a short break to look at some cute little puppies.

Elimination periods

In addition to the criteria above, you must reach the end of your elimination period, the waiting time before your insurance kicks in.

For example, if you have a 90-day elimination period, your benefits don't start until after you need 90 days of care.

Why is it called an elimination period? There's no good reason. It sounds like something an '80s action hero would say.

A better name could’ve been "waiting period" or "benefit delay," but here we are. Think of it like your insurance deductible—only with days instead of dollars.

Check your policy for how your elimination period works.

- Some start after a physician's review while others after care begins.

- Some are cumulative, while others require consecutive days.

- Most policies only require that you meet the elimination period once. If you no longer need care for a few years and then start again, the requirement is usually waived.

Benefit period

The benefit period is the number of years your LTCi policy will cover you once you need care—usually ranging from 2 to 8 years.

How benefit periods work

Benefit periods are calculated differently based on your policy type:

- Traditional policies: Your benefit period depends on how much of your LTC coverage you use each month.

- For example, if you have a 4-year benefit period with $6,000/month coverage but only need $3,000/month, the unused $3,000 is carried forward each month.

- This effectively extends your benefit period, potentially doubling it to 8 years (assuming you don't pass away first).

- Hybrid policies: Your benefit period is fixed since most hybrids pay you the full benefit in cash.

Optimal benefit period length

More years sound better, right?

Think of the benefit period as the number of years your LTC policy holds onto your money before paying it out.

For example, if you select an 8-year benefit period, you would need 8 full years of care to maximize your benefits. If you pass away earlier, any unused benefits are lost.

In most policies, a longer benefit period means more potential benefits, but it also comes with a lower chance of receiving them all.

When comparing policies, remember: you pay for LTC costs in money, not years.

Other considerations

- Women typically need LTC longer than men do (3.7 years vs. 2.2 years). This difference may influence your decision.

- Some policies offer unlimited length benefits, but these come at a higher cost. Below, we review policies that include unlimited length options.

Tax benefits

Long-term care insurance comes with some nice tax perks—like the fact that benefits are usually tax-free.

Some policies break out separate premiums for the life insurance and long-term care portions. That can help you save on taxes when you buy the policy.

See our post on tax breaks to learn more.

Wrap up

If you live in Colorado like I do, having all-wheel drive really matters—it’s a feature that fits the way we live.

Long-term care insurance should work the same way. The features should fit your life and what you care about most. You might prioritize:

- low annual payments,

- the most flexible coverage for home care, or

- longer coverage in case of memory care.

Your future self will thank you for making smart decisions now.