Jeff and Shannon,

Your long-term care insurance quotes are ready.

You asked to see policies with longer benefits, no refund, and 5% benefit growth. To help you evaluate options, I’ve focused on two popular policies.

• NGL EssentialLTC - A traditional joint policy that provides 6 years of benefits for each of you, plus an additional shared bonus pool of 6 years. There is no refund if care is never needed.

• OneAmerica Asset Care - A hybrid joint policy that offers uncapped lifetime benefits, along with a small refund if care is never needed.

Treat these numbers as a first draft. We can refine them as we narrow in on the policy and structure that fits you best.

↗️ Benefit growth

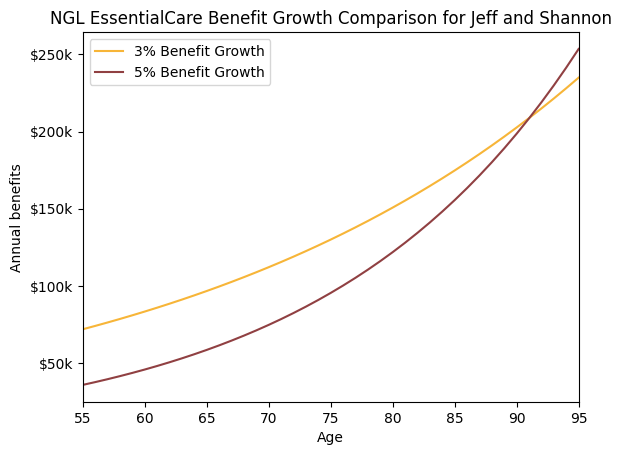

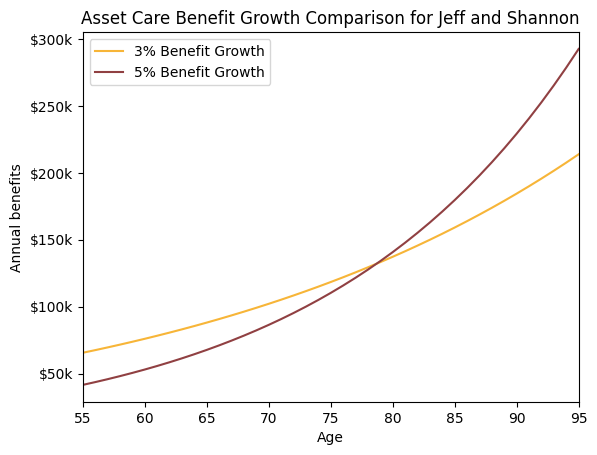

You asked to explore 5% inflation protection, which is smart to consider versus 3%. For the same premium, 5% benefits start lower than 3%, but grow faster over time. Each insurer chooses where to start these lower benefits.

A helpful way to compare them is the crossover age, which is the point at which the 5% benefit becomes larger than the 3% benefit. To compare, I created a few graphs comparing the two options using the same premium.

NGL EssentialLTC - 5% growth wins if you need care after age 92

OneAmerica Asset Care - 5% growth wins if you need care after age 79

As you probably noticed, 5% growth with NGL "costs" more.

🔎 Your quotes

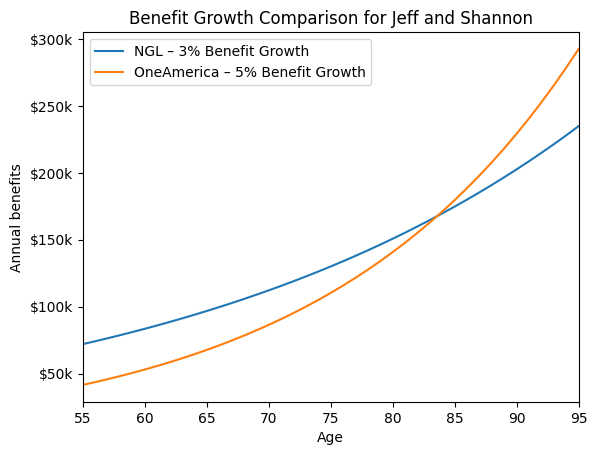

The quotes below use the same $25k/year premium paid for 10 years to enable a clean comparison. You can increase or decrease the premium, and the benefits will scale proportionally. Benefit growth was selected for each policy based on crossover ages, for example, NGL is most competitive with 3% growth. Benefits can begin at any point, even before premium payments are complete. For illustration, future benefits are shown at age 80, a common age when claims begin.

🧐 My notes

Below are some thoughts on how you might think about your choices.

What offers more benefits?

Let's compare the annual benefits of these two policies over time. Using the same premium, the OneAmerica policy provides higher benefits if care is needed after age 84. Most long-term care needs occur later in life, but the timing is unpredictable and varies by individual.

What payment schedule?

These results can shift somewhat depending on the payment schedule you prefer.

NGL - Offers single-pay, 10-year, and lifetime payment options. Lifetime payments are not contractually guaranteed and can increase over time, though lifetime payments generally produce the strongest benefits from NGL.

OneAmerica - Offers a wide range of payment options (once, 5y, 10y, 20y, to age 95), all of which are contractually guaranteed and will not increase. The strongest benefits are typically achieved with shorter payment schedules, especially a single payment.

Is this the right amount of coverage?

Assisted-living in North Carolina is projected to cost $211,000/year by age 80 (assuming 4% annual growth). Your options provide lower annual benefits ($135k-$150k/year) than this projection, but you can bridge the gap using personal savings and Social Security. The goal for most people is meaningful coverage, not paying every dollar.

Wrap up

Choosing the right policy ultimately depends on your priorities and practical constraints. We can review these options and any others on a call, but this should help frame the decision and clarify the tradeoffs.

👉🏻 Next steps

If any of these policies look appealing, please schedule time on my calendar so we can review the options together and address any questions you may have.

📺 Still learning?

Watch our "unboring" video on qualifying for LTC insurance or visit our website. That's me in the video.

Thanks,

Jesse

Jesse Vickey at Long Term What?

Schedule a call or 720-263-2188