📺 Watch this and other posts on YouTube or listen on Spotify, Apple Podcasts, and YouTube Music.

Intro

People often ask, how much does long-term care insurance cost?

The short answer: it’s tough to say. It’s like asking a realtor, “What does a house cost?” It depends, but in this post I’ll show what drives the price and give a few real examples.

Post jargon

benefit: the amount LTCi pays for covered care expenses

death benefit: a payout to a beneficiary from a hybrid policy after the insured passes away

inflation protection: LTCi benefit that adjusts for rising costs

LTC: long-term care

LTCi: long-term care insurance

premium: the payment to maintain insurance

➡️ Explore all the LTC jargon

Name your price

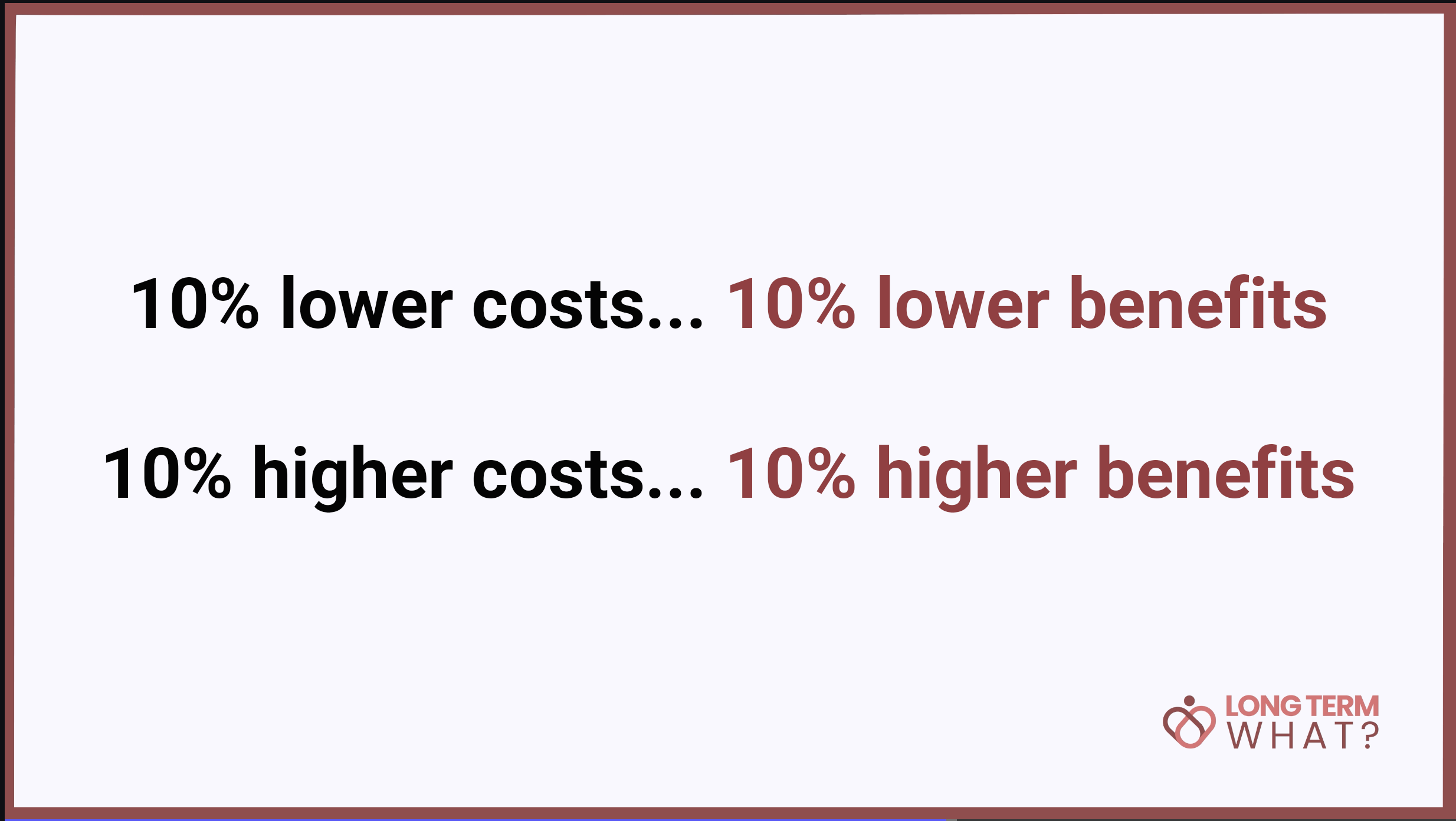

First, you can name your price. Remember the game show The Price Is Right, back when Bob Barker was the host? Contestants got to name their price.

Long-term care insurance works the same way. There's no preset gold, silver, or bronze plan.

Let’s say you get quotes from us. You could lower your costs and your benefits would drop by about the same amount. Or you could increase your costs and your benefits would rise about the same amount. You name your price.

As you name your price, remember that insurance doesn’t have to cover every last dollar. Many people get meaningful coverage—enough to ease the cost, but not to cover the whole thing.

Payment options

Once you’ve set your budget, the next question is how you want to pay. Some policies let you pay once and be done. For others, you can spread payments over 5, 10, or even lifetime terms. The longer you stretch it, the more you’ll pay overall.

And here’s an important detail: not all policies guarantee that your cost will stay the same each year.

Some older policies were cheaper up front, but their premiums have gone up over time. We can show you policies that guarantee your costs will never go up.

How the price is determined

Next—let’s discuss the factors that go into the price. The price varies on you. Women typically pay more because they live longer.

Costs also rise each birthday and with certain health conditions.

You can also spend more to add various options or riders to your policy. One of the biggest options is how you want your benefits to grow—3% or 5% a year—to keep up with care costs.

There are about a dozen strong insurers offering coverage, each with different sweet spots. Some have better options for women in their 60s or if you’re in physical therapy. That’s why it’s always smart to shop different policies.

No matter where you buy, us or any broker, the cost is the same. Insurers set the price, so it helps to shop insurers, but not agents, for the right price.

Tax perks

Long-term care insurance offers lots of tax perks. Benefits are typically tax-free when you receive them. And if you’re a business owner, what you pay can often be tax-deductible—especially for C-corps. In other words, you’ll pay less.

General quotes

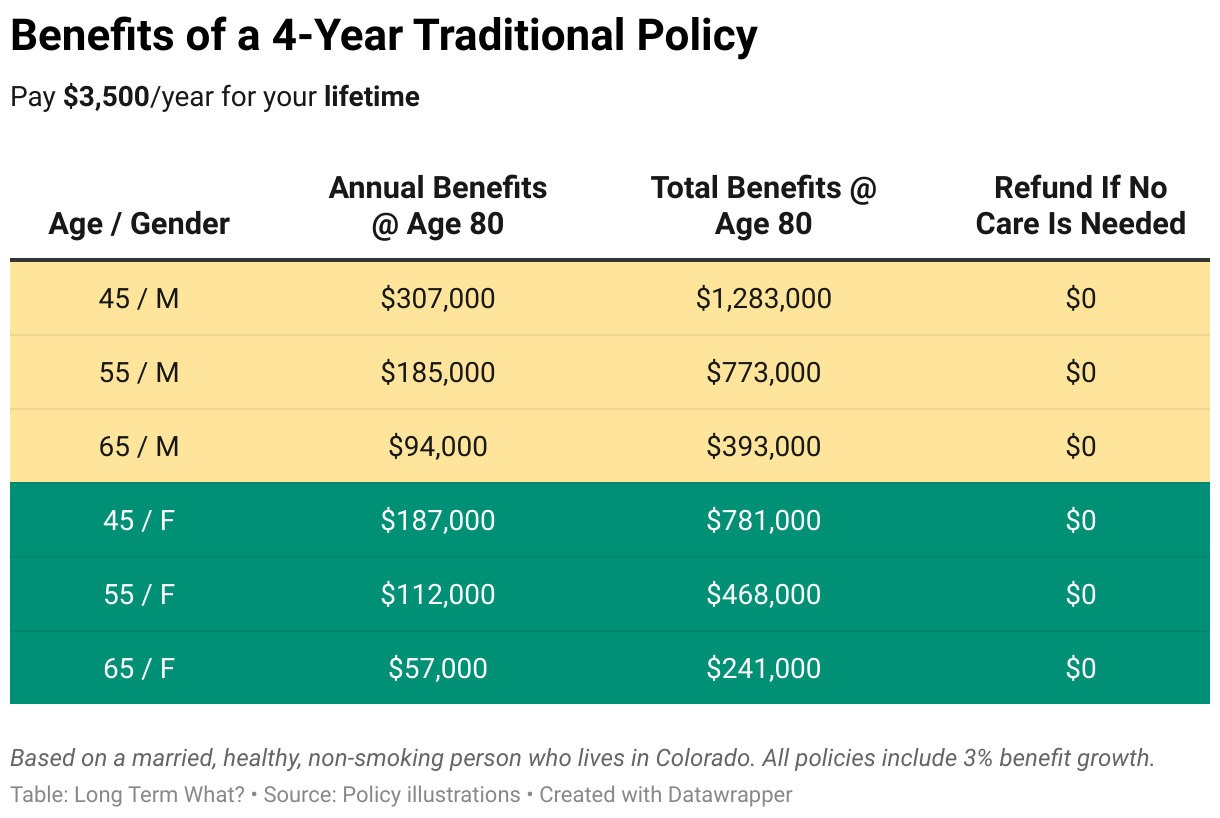

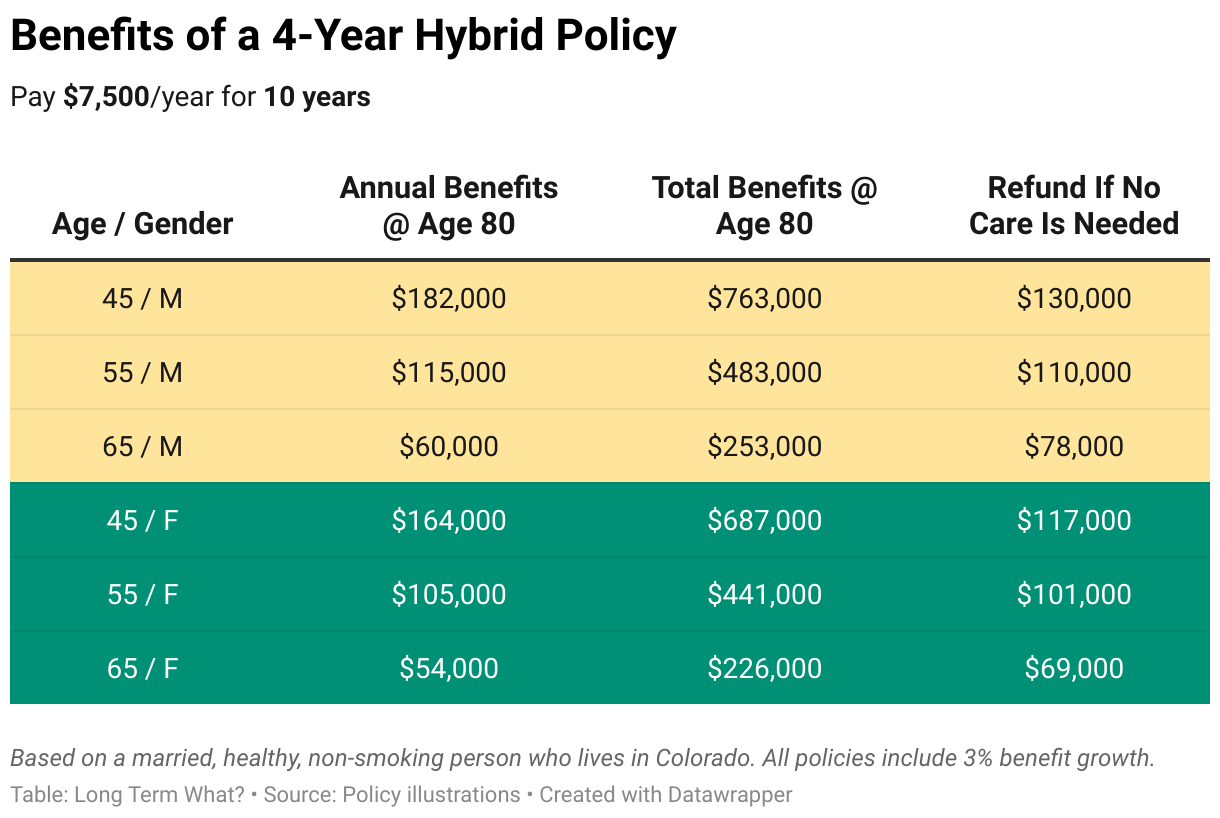

Below are general quotes from popular traditional and hybrid policies.

Pricing calculator

📝 Other Notes

- If two people need coverage, you may qualify for discounts through a joint policy or by pairing two individual policies with partner discounts.

- The minimum you can spend on LTCi is $100/month for a traditional policy or a $50,000+ lump sum for a hybrid policy, with high-end options exceeding $500/month or $300,000+.

Wrap up

Kudos to you for taking an important step toward understanding the pricing of LTCi. Most people don’t start this process until it becomes urgent, but planning ahead puts you in control.

The pricing calculator above reflects just one popular policy, but we offer the best policies on the market. Costs and benefits vary, so explore multiple options to pick the policy that makes you ecstatic.

If LTCi feels like part of your plan, consider buying sooner rather than later. Purchasing earlier reduces the chance of being declined for coverage, ensures your coverage starts now, and saves you money.

Remember, when it comes to LTCi, the price can be right for you—no Big Wheel required.