Winter,

Good news. Your revised long-term care (LTC) insurance quotes are ready.

LTC costs in Georgia

Let’s begin with what care might cost. Assisted-living in Georgia is projected to cost $253,000/year by age 80 (assuming 4% annual growth). But your policy doesn't have to cover everything. Assisted-living already includes housing and meals, and any steady income, like Social Security, can bridge the gap that your policy doesn't cover.

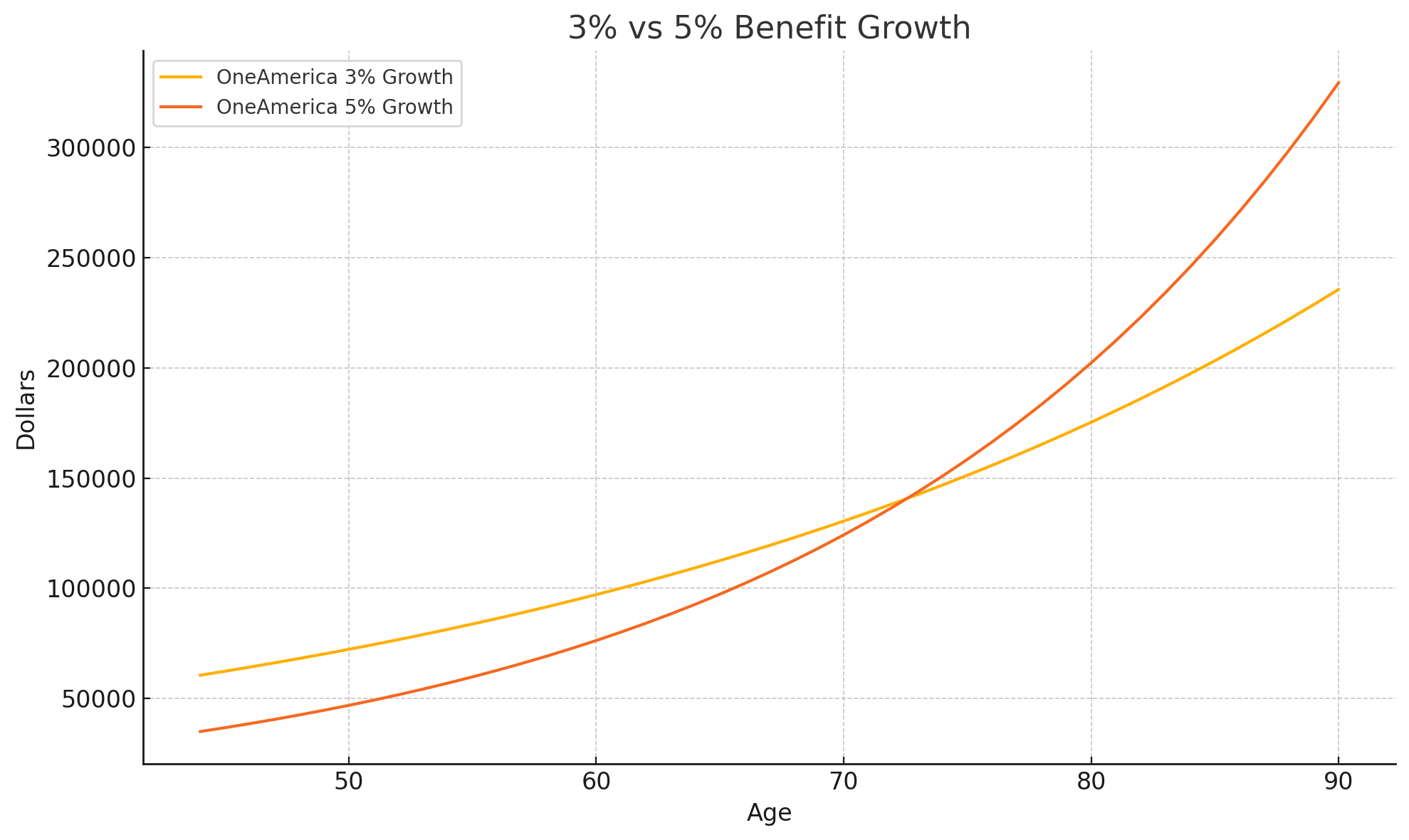

Benefit growth

Before I show you quotes, let's consider growth options. Since you're applying for long-term care insurance at a relatively young age (which is great!), it's worth considering how your benefits will grow over time. Historically, long-term care costs have increased by more than 4% annually over the past two decades. Here are two good options for benefit growth:

- 3% → Provides solid coverage that keeps up with inflation moderately well.

- 5% → Starts with lower coverage, but grows faster—giving you significantly more coverage later in life, when the need for care is more likely.

In the graph below, notice how the 5% growth policy (red line) starts below the 3% policy (yellow line), but overtakes it around age 72.

👀 Revised quotes (v2)

Since your goal is to cover the potential cost of long-term care, I’ve included a few options that offer extended coverage for conditions like Alzheimer’s. These are designed to align with your expected care costs—about $253,000/year by age 80 in Georgia. In the table, I bolded key changes as you move from left to right across the columns.

🧐 My notes

All include a refund. Here’s why I chose these options for you:

A – Your original Cadillac pick. Strong annual benefits, but still less than half your expected LTC costs.

B – Switched to a single payment to boost benefits.

C – Increased your annual costs from $8,500 to $15,000 to show how benefits grow with a higher payment.

D – Changed the benefit growth to 5% to show stronger benefits by age 80.

E – Swapped to Nationwide CareMatters with a 7-year benefit period—lower cost and higher benefits at age 80.

🔑 Here are your key decision points:

Growth rate: Do you want 5% growth (higher benefits later, lower earlier)

Budget: Do you prefer to pay over 10 years, 5 years, or once?

Memory care: Is lifetime coverage worth it, or is 7 years enough? (7 years is about twice the average claim length for women, though memory care can last 8+.)

🎯 Personally, I think Option E strikes a great balance: lower premiums, strong benefits, and a long benefit period.

🏢 Related, if you own a business and pay through it, you may qualify for several tax breaks that can significantly reduce your out-of-pocket cost.

👉🏻 Next steps

Just reply to my email or text with A, B, C, D and/or E with any notes and I’ll email the policy documents (no commitment).

📺 Still learning?

Watch our 7-minute "unboring" video on the features of LTC insurance. That's me in the video.

Thanks,

Jesse

Jesse Vickey at Long Term What?

Schedule a call or 720-263-2188

Website | YouTube | Email