Ryan,

I'm pleased to offer three long-term care insurance (LTCi) quotes that provide meaningful coverage.

Comparison table

✨ All policies include:

- Flexible care: at home or in a facility

- Adjustable premium and benefit options

- Starting benefits when you qualify for LTC

View local care costs here.

Graph of benefits

This graph shows how your benefits would compare to expected LTC costs if you needed care at age 80. Click any policy name or line for more detail.

My thoughts

Based on your preferences:

- Memory care (unsure): OneAmerica offers lifetime benefits, which can be ideal for longer-lasting memory care needs. However, the annual benefit amount is lower compared to others.

- Refund (yes): All three policies include a death benefit, meaning if you never need care, your heirs receive more than what you paid into the policy.

- Need smaller payments (no): Nationwide and Securian are usually close in competitiveness. In this case, Securian's benefits appear lower because I quoted it as a 10-pay, whereas Nationwide was structured as a single lump sum.

How I can help

- Want to adjust the costs or benefits for any plan? Just reply and I’ll send revised quotes.

- Want the full brochures? Just reply to my email and I'll send them over.

- Have questions? Just reply, text me at 720-263-2188, or grab a time for a quick call here.

Thanks,

Jesse

Version 2 - May 12, 2025

Ryan and Victoria,

Thanks for taking the time to speak with me today. As promised, I’ve included some comparisons below for your review. I’ve broken them out into a few key decision points to help make things easier.

Securian or Nationwide?

Some thoughts:

- Zooming in on Ryan's comparison:

- Securian: He'd receive $35,387 more in total benefits ($1,133,379 - $1,097,992) if he needed 6 years of care.

- Nationwide: After meeting the 90-day elimination period, the policy pays retroactively for those first 90 days of care—worth $34,224 at age 80—so benefits essentially start from day one (and end 3 months earlier). From that point forward, it continues to pay for all eligible care. It also includes an extra $19,676 in guaranteed minimum life insurance.

- While the odds of receiving any of these benefits are unknown, Nationwide’s are statistically more likely.

- The same takeaways apply to Victoria’s options as well.

- Zooming in on Victoria's comparisons:

- I used $5,000/year for her premium (50% of Ryan’s).

- Her projected benefits are less than 50% of his, since policies cost more for women due to their higher average care needs (3.7 years vs. 2.2 years).

- If Victoria wanted more or fewer benefits, we could adjust her premiums proportionally—for example, a 10% increase in premiums would result in roughly a 10% increase in benefits.

My thoughts: It’s a close call, but I’d lean slightly toward Nationwide, since the odds of receiving those added benefits are higher.

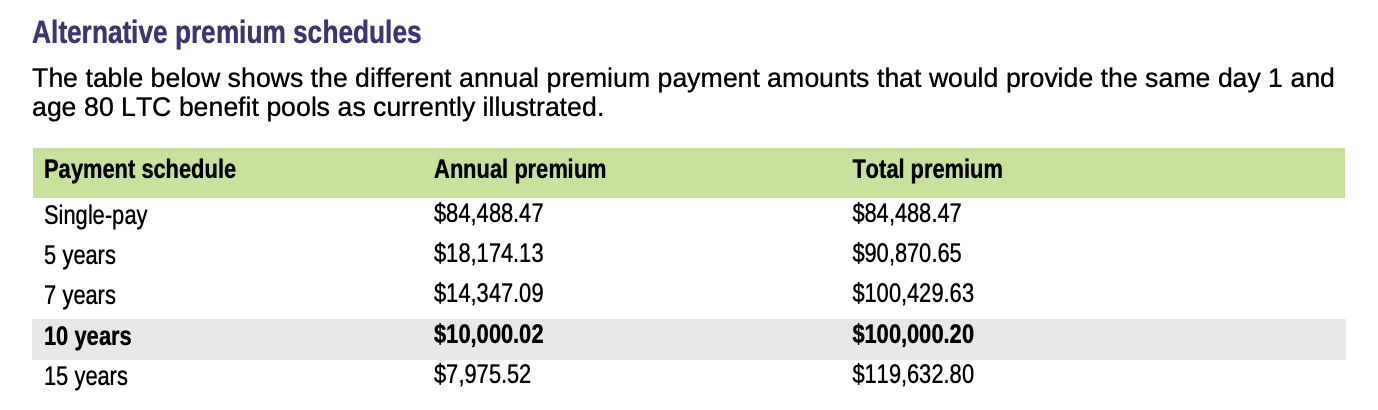

What premium schedule?

On page 13 (page 12 of 17 in the PDF), Securian shows alternative payment options that provide the same benefits:

Nationwide doesn’t include this table in their illustration, but they offer similar flexibility: single-pay, 5-pay, 10-pay, pay to age 65, and pay to age 100. For the same benefits:

- Pay to age 65 ≈ 85% of 10-pay (e.g., $8,482/year vs 10-pay of $10,000/year)

- Pay to age 100 ≈ 53% of 10-pay (e.g., $5,291/year vs 10-pay of $10,000/year)

Premium waivers

- Nationwide: If either of you goes on claim (i.e., begins receiving benefits) and is on the “pay to age 100” schedule, the LTC portion of the premium (roughly 40%) would be waived.

- Securian: You can pay extra to add a full premium waiver rider if you go on claim. Let me know if you’d like quotes for this option.

My thoughts: I’d go with the shortest payment schedule you can reasonably afford.

Individual or joint?

As we discussed on our call, Nationwide offers a joint policy that covers both of you under one contract. You’d share a total of 8 years of coverage, which adds some flexibility—for example, Victoria could use 7 years and Ryan 1 year, or any other combination that adds up to 8.

It’s worth comparing this to the alternative: two individual policies, where each of you has separate, dedicated benefits.

My thoughts:

- After reviewing the quotes, I don’t recommend the joint (“Together”) policy. The individual policies generally offer stronger benefits across most/all comparisons.

- With the joint policy, the life insurance (death benefit) isn’t paid out until both of you pass away. In contrast, the individual policies pay out after each death (better).

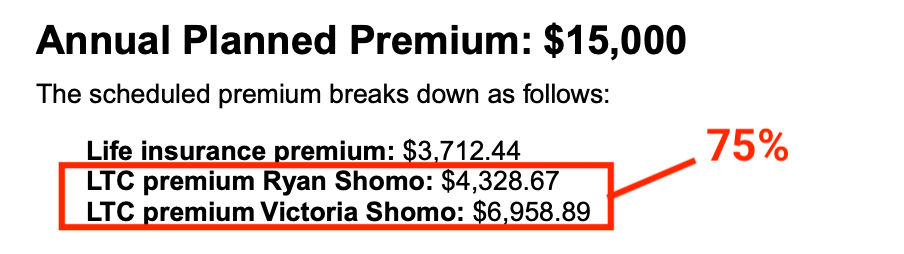

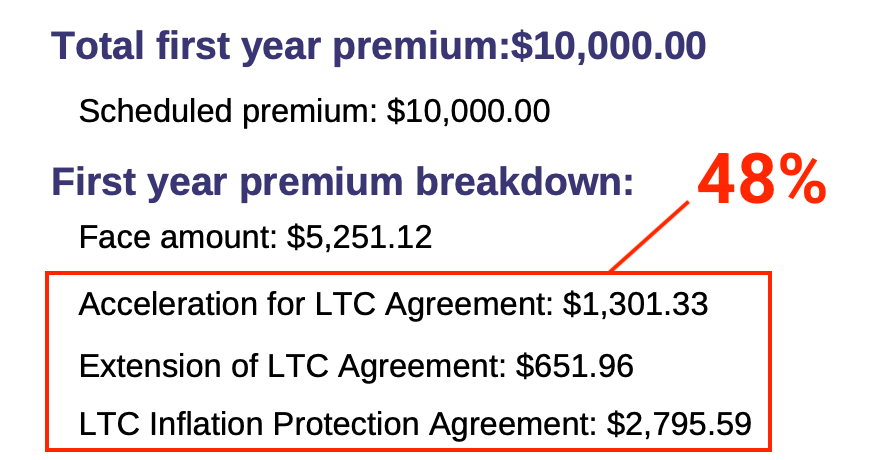

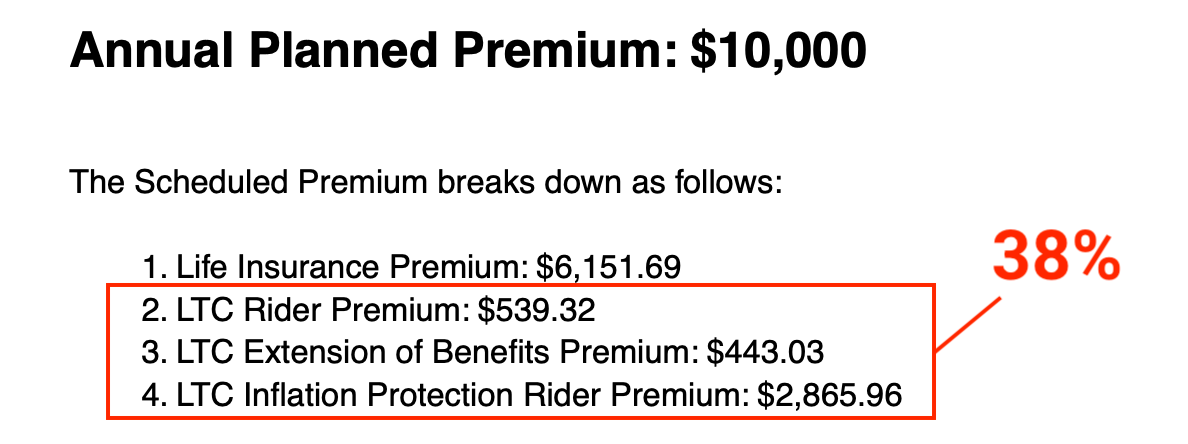

- The only real advantage I see to the joint policy is a higher percentage of the premium being allocated to LTC benefits (see below)—but I doubt that would outweigh the downsides.

Pay from your business?

You mentioned that you're business owners. If you pay for the policy through your business, you may qualify for special tax advantages.

Both Nationwide and Securian break down their premiums into separate components. The higher the percentage allocated to LTC (long-term care), the greater the potential for tax deductions—especially important if you're structured as a C-Corp.

My thoughts: The financial benefit in tax treatment isn’t dramatic, but it could be a slight tie-breaker. If you have a C-Corp, the potential tax savings are most significant.

Summary

After reviewing your options, I’d recommend going with two individual policies—either from Securian or Nationwide, for the higher benefits.

Timing

Since Ryan’s birthday is July 15, his policy cost will go up slightly after that date. To lock in the current rate, the application just needs to be signed and submitted by then—no payment required yet.

Purchasing direct

You also mentioned that the Securian quote you received directly was a bit different from mine. I double-checked—Securian pricing is always the same whether you go through a broker or buy directly. The difference is likely due to a variation in inputs. If you’d like, you can:

- Compare their quote to the attached illustration I provided, or

- Email me their version and I’d be happy to do a side-by-side comparison for you.

What's next

Once we're settled on the best policy design:

- I can do another quick health check-in to make sure there aren’t any surprises—like pending procedures, recent physical therapy, steroid injections, or anything else that could delay or complicate approval.

- I’ll guide you step-by-step through the application process.

- From start to finish, most applications take about 2 to 6 weeks to complete, depending on how quickly the phone interview is done and whether underwriting needs follow-up info.

Let me know if you have any questions—I’m happy to help over email or schedule another quick call.

Thanks again,

Jesse