Heather,

Thanks for speaking with me. Your revised long-term care (LTC) insurance quotes are ready.

📃 Your current policies

Thanks for sharing your current policies. Below are some of my thoughts.

Midland National policy

You're right. Your policy’s cash value is about $1,039. A 1035 exchange is most useful when the cash value is higher than the total premiums paid, since it helps avoid taxes on any growth. In your case, you’ve likely paid around $6,500 into the policy, so there’s no taxable gain and no tax advantage to using a 1035 exchange.

If you want to apply the value of this policy toward your new coverage, you can simply cancel the policy, receive the $1,039, and use those funds for the new policy. A 1035 exchange isn’t needed here.

New York Life LTC policy

This one is great! Your policy was issued in December 2022 and provides 4 years of long-term care benefits starting at $1,500 per month, along with a $36,000 death benefit if no LTC benefits are used. With the 3% compound inflation protection, your annual LTC benefits at age 80 would be roughly $55,000/year paid as reimbursement. 👍🏻

🎯 Your target

Assisted living in Texas is projected to cost about $259,000/year by age 80 (assuming 4% annual growth). Memory care typically runs about 20% higher.

Most people aim for meaningful coverage rather than covering every dollar. A common target is 70% of future LTC costs, which for you translates to roughly $180k/year (assisted living) to $215k/year (memory care) at age 80. For simplicity, we can use $200k/year as your planning target.

At age 80, your New York Life policy provides roughly $55k/year for 4 years, which leaves the following coverage gaps:

- Years 1–4: $200k/year target − $55k/year benefit = $145k/year gap

- Years 5+: $200k/year gap (no remaining LTC benefits)

These numbers are directional, not precise, but they give us a clear starting point for choosing the right level of additional coverage.

🔁 Revised quotes

For OneAmerica using 5% growth, the minimum payment is about $600/mo, so I priced all the policies at $600/mo to provide an apples-to-apples comparison.

🧐 My notes

Adding the New York Life benefits is meaningful. You'll always need earlier benefits (years 1-4) than later benefits, so these extra benefits are helpful.

The question is how to layer a second policy onto your New York Life benefits in the best way.

Options A, B, and C (Nationwide)

If you purchased a Nationwide policy, your benefits would be paid in cash. This avoids the risk of overinsuring your first four years alongside your New York Life policy, since any unused Nationwide cash benefits can simply be saved for later years. Depending on the benefit period you choose, you can also reduce your premium from the $600/mo range. Read the review.

Option D

OneAmerica Asset Care provides lifetime benefits and is widely regarded as the gold standard for long-duration coverage. The minimum premium for this structure is about $600/mo. Because the policy is primarily reimbursement-based, there is a chance you may not use the full combined benefits available in years 1–4, and then be underinsured in later years when your New York Life benefits have ended. Read the review.

👉 My suggestion: I think your best fit is Option E (Nationwide for 7 years) with a $500/month premium.

- Years 1–4: Combined with your New York Life policy, you’d reach roughly $200k/year in total benefits, which matches your target.

- Years 5–7: Your New York Life benefits would be finished, but Nationwide would continue providing strong coverage through the later years of a claim.

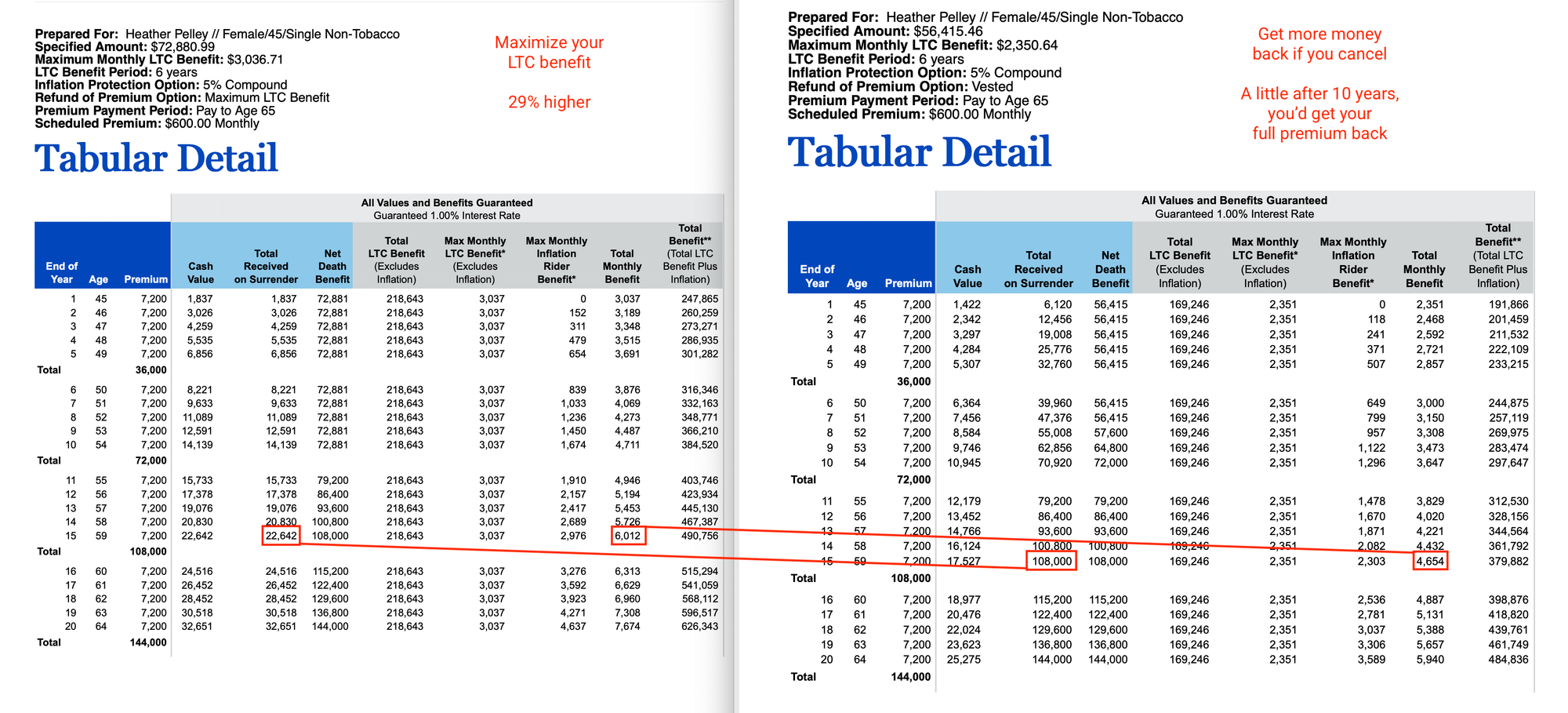

♻️ Money back option

If you want the option to receive more money back if you cancel the policy early, I priced a 6-year option with Nationwide for comparison.

- Maximize your LTC benefit = About 29% higher benefits

- Maximize your money back if you cancel = You would receive your full premium back after roughly 10 years

You can click the image to enlarge it. If your goal is to maximize your LTC benefits, I wouldn't recommend this option. But it's a nice fit if you feel like you might cancel the policy.

👉🏻 Next steps

With the New York Life policy, you have a few things to consider. Let's talk again whenever is convenient. Grab a 15-min call.

📺 Still learning?

Watch our "unboring" video on qualifying for LTC insurance. That's me in the video.

Thanks,

Jesse

Jesse Vickey at Long Term What?

Schedule a call or 720-263-2188

Website | YouTube | Email