Sandra,

Thanks for our call today. After reviewing your quotes, I revised them to give you a clearer way to compare your options.

🔁 Revised quotes

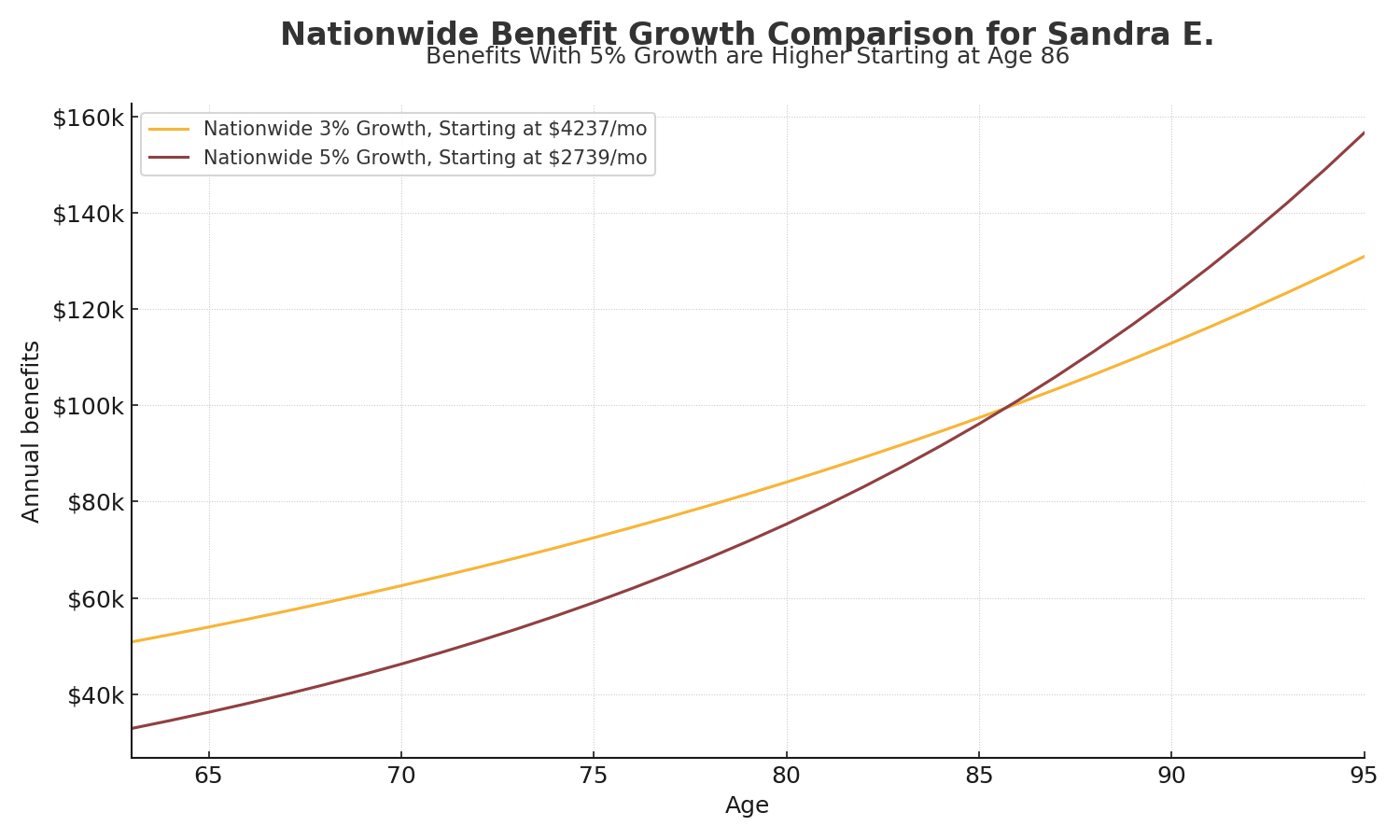

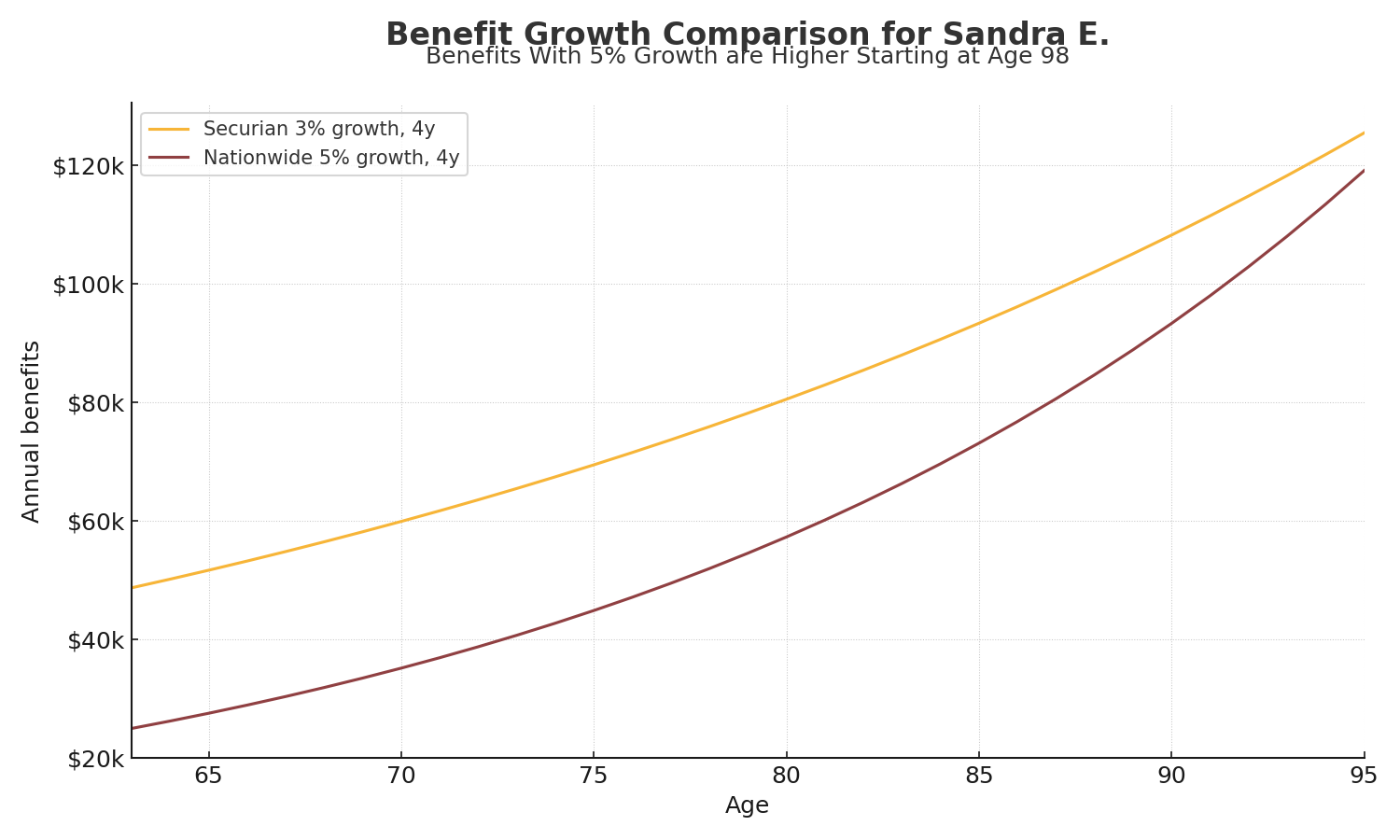

To help you make the best decision, I updated your quotes so each option now uses the same premium. This creates a true apples-to-apples comparison.

Earlier we looked at 3% versus 5% breakeven graphs, but the premiums differed, which made the comparison harder. Using equal premiums gives you a clearer view of how the benefits stack up. 👍🏻

This first comparison looks at the two 3-year Nationwide policies (A2 and A3). With equal premiums, the 5% benefit growth wins after age 86.

In the two 4-year policies with equal premiums (A4 and B), the 5% policy wins at age 98.

🧐 My notes

Based on these updated graphs:

- If you prefer a 3-year policy, I'd probably choose the Nationwide 3% option because the breakeven is much later (age 86).

- If you prefer a 4-year policy, I'd choose Securian with 3% growth.

Between these two choices, I'd probably go with the 4-year Securian with 3% growth since the total benefits are fair bit higher.

You can then adjust your premium up or down from $850/mo based on your budget.

👉🏻 Next steps

Once you pick your preferred policy and premium, let me know and I'll send you an updated policy illustration with precise numbers. Then we can start your application. 👍🏻

📺 Still learning?

Watch our "unboring" video on qualifying for LTC insurance. That's me in the video.

Thanks,

Jesse

Jesse Vickey at Long Term What?

Schedule a call or 720-263-2188

Website | YouTube | Email