Vishal,

Good news. Your revised long-term care (LTC) insurance quotes are ready.

🔁 Revised quotes

I’ve provided three options comparable to your Plus and Cadillac choices (hybrid policies with guaranteed premiums and refunds). Each uses a $100k single premium for an apples-to-apples comparison with additional payment options listed below the table. You can also raise or lower the premium and the benefits will adjust proportionally.

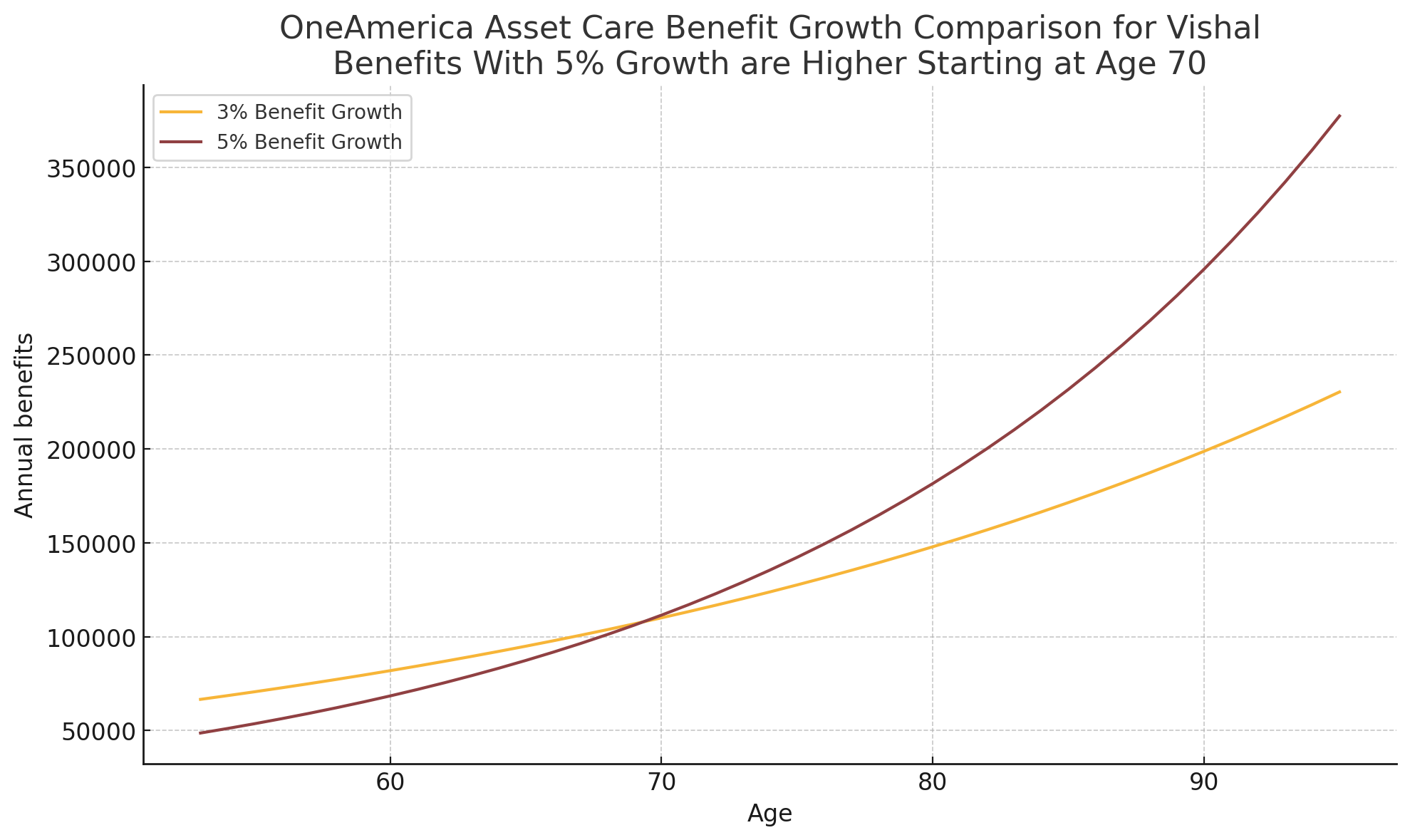

OneAmerica - Below is a comparison of the annual benefits for the OneAmerica policy with 3% (option C) and 5% (option D) growth.

The 5% (red) line surpasses the 3% line at age 70. Because most long-term care needs arise after age 70, I recommend the 5% option (the policy is attached). The tradeoffs are a lower death benefit ($97k vs. $133k) and lower benefits before age 70.

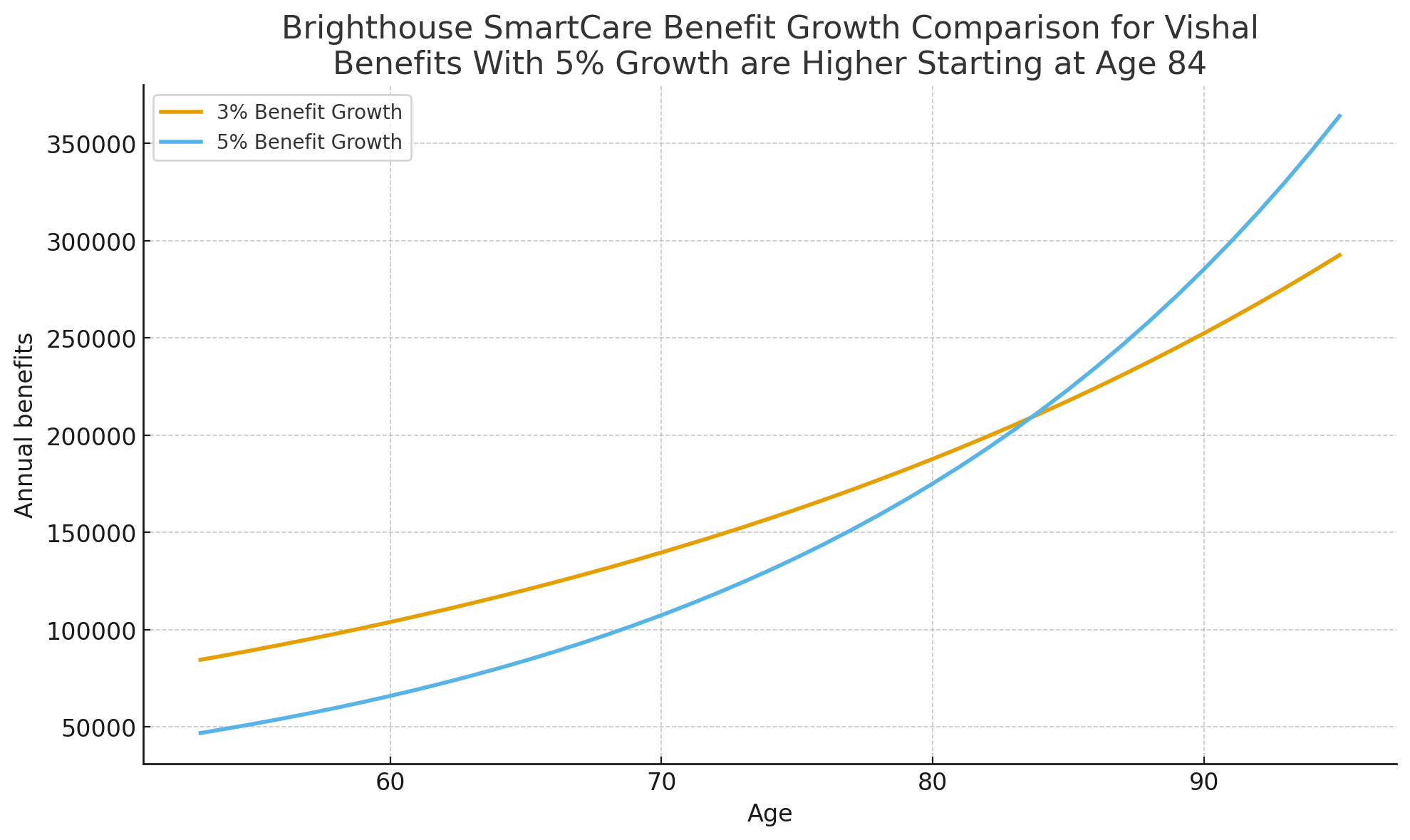

Brighthouse - Below is a comparison of the annual benefits for the Brighthouse policy with 3% (option A) and 5% (option B) growth.

The 5% (blue) line surpasses the 3% line at age 84. With Brighthouse, the higher growth option is harder to justify because the crossover comes so late. I would lean toward the 3% option.

💵 Payment options

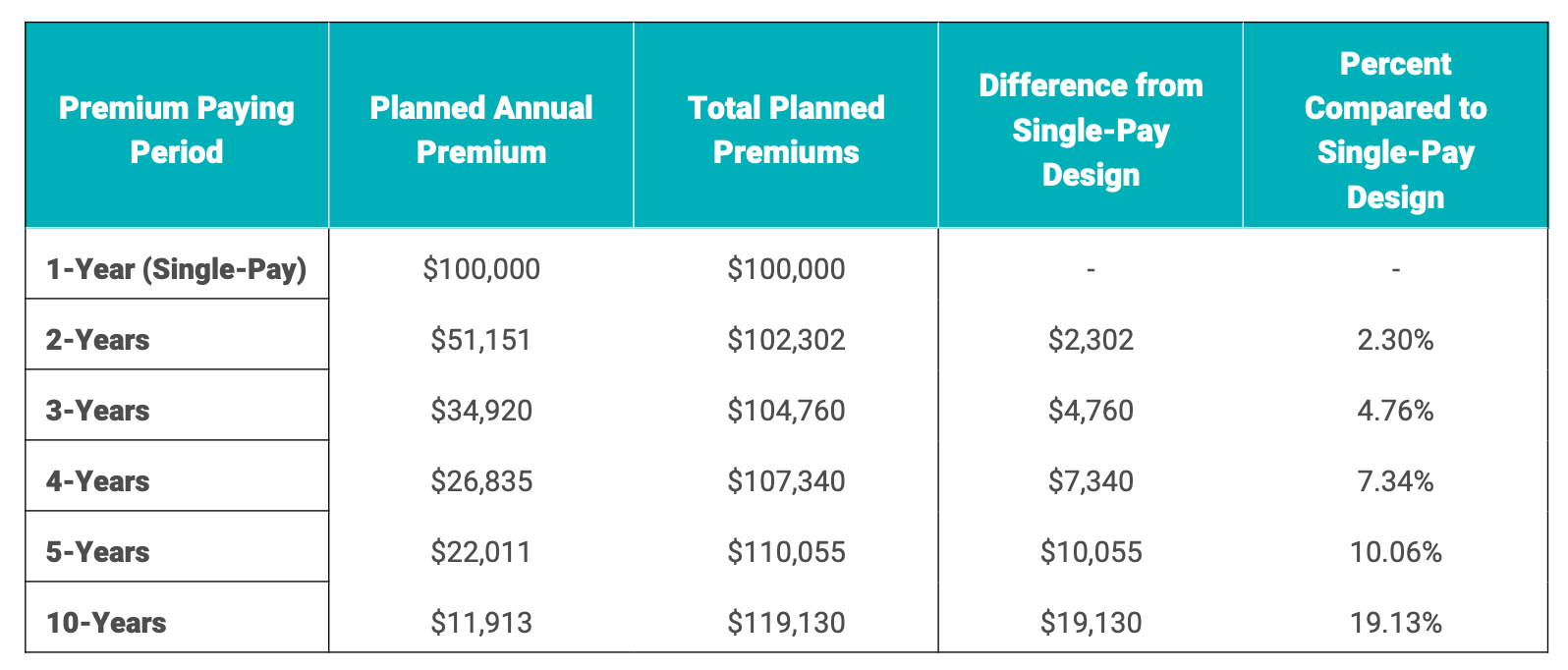

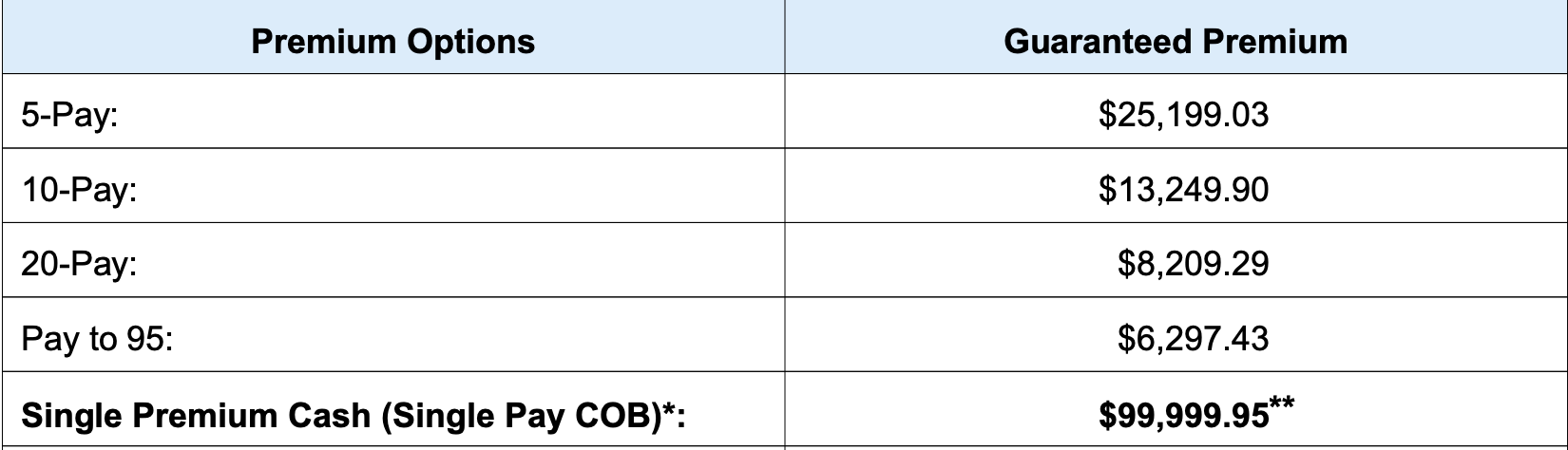

The following payment options—rather than a single $100,000 payment—come from your policy documents.

Option B - Brighthouse (on claim, premiums stop)

Option C - OneAmerica (on claim, premiums stop)

🧐 My notes

Based on our discussions, I think these are your two best choices:

Option A (Brighthouse at 3% growth) - My review

You would receive 100% cash benefits anywhere in the world. Benefits last six years, which is meaningful coverage even if it does not cover every possible scenario. If you receive care abroad, costs would likely be lower. Choose this policy if international benefits are very important.

Option D (OneAmerica at 5% growth) - My review

You would receive lifetime benefits to cover memory care and other long-duration needs. This policy adds little value for international care but provides strong peace of mind for long-term care in the US. Choose this policy if benefits beyond six years are most important to you.

Assisted-living in Pennsylvania is projected to cost $211,000/year by age 80 (assuming 4% annual growth). Your options provide lower annual benefits than this projection, but you can bridge the gap using personal savings and Social Security. The goal for most people is meaningful coverage, not paying every dollar.

If you'd like higher annual benefits, you can increase your premium—your benefits will rise proportionally (e.g., by 25%).

👉🏻 Next steps

We can discuss these options on our upcoming call.

I also recommend completing this longer health pre-screen form (10 minutes). I’ll share your answers anonymously with insurers to get informal feedback before any formal application. This helps us identify which policy is the best fit and avoids the risk of a formal decline.

📺 Still learning?

Watch our "unboring" video on qualifying for LTC insurance.

Thanks,

Jesse

Jesse Vickey at Long Term What?

Schedule a call or 720-263-2188

Website | YouTube | Email