Kevin and Melissa,

Below are your long-term care (LTC) insurance quotes and a short explanation of how I determined each option.

💰 How much insurance?

First, I like to start with a target. In 30 years, when you're both in your late 70s, the average cost of assisted living in Austin is projected to be around $259,000 a year, assuming a conservative 4% annual growth. For meaningful coverage, I’ll target benefits of about 70%+ of that amount: $186,000/yr ($15,500/mo) in 30 years. Some quoted benefits are a little higher.

This is just a working estimate. We can adjust the coverage up or down based on your preferences.

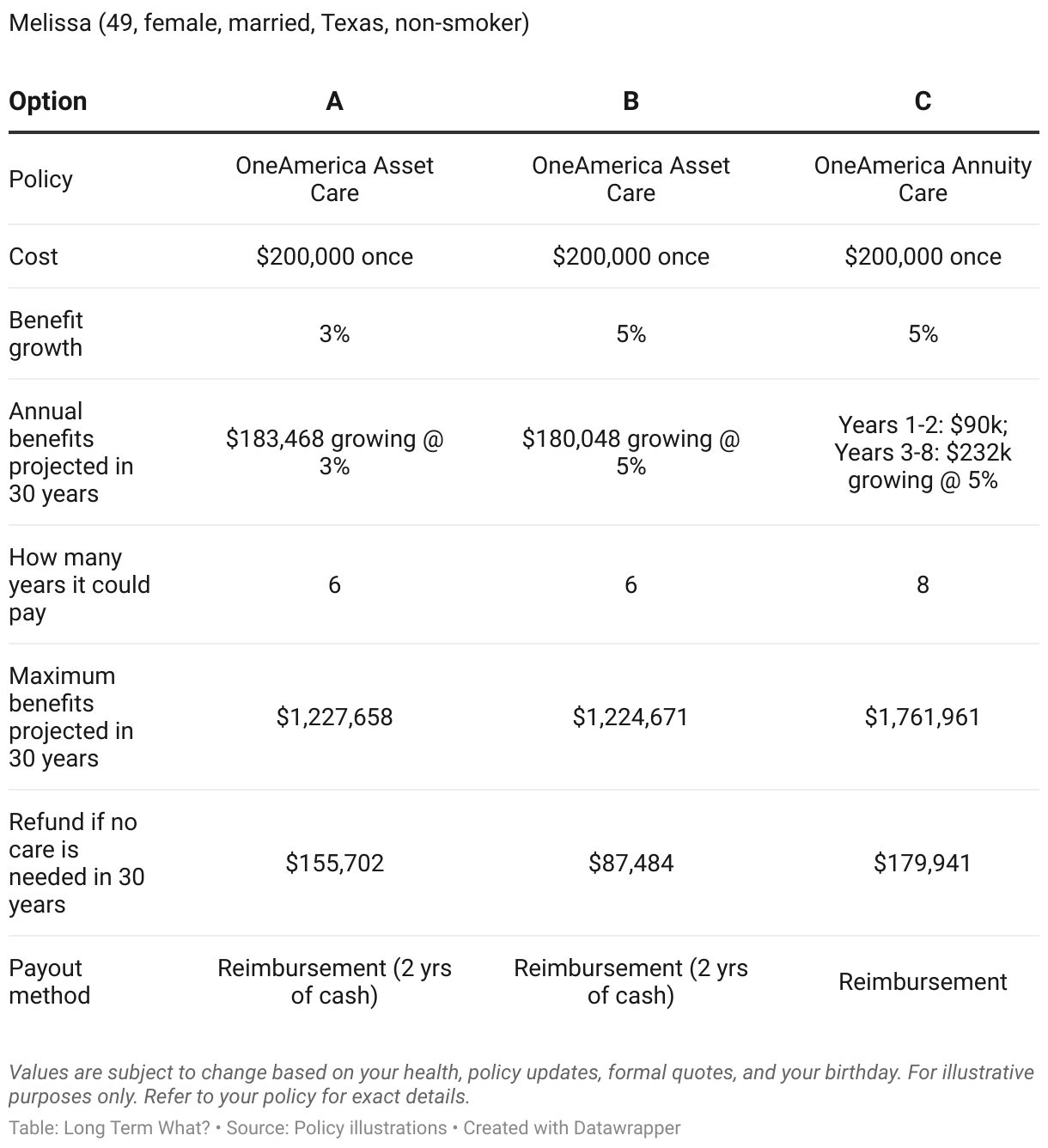

🔎 Melissa quotes

Based on Melissa’s health history, we have two viable paths:

- Life/LTC Hybrids: Unfortunately, no insurers could offer coverage except OneAmerica Asset Care, which may approve her at a lower rating (table 6, or lower) and limit her benefits to a maximum of six years.

- Annuity/LTC Hybrids: She would qualify for annuity-based options. As we discussed, these typically offer lower benefits than life/LTC insurance, but OneAmerica Annuity Care is fairly comparable (or even better) to OneAmerica Asset Care's quote. I'm waiting on underwriting feedback on a second annuity option as well.

In the table below, I've provided quotes for two versions of Asset Care (3% growth and 5% growth) at the lower rating plus Annuity Care (5% growth).

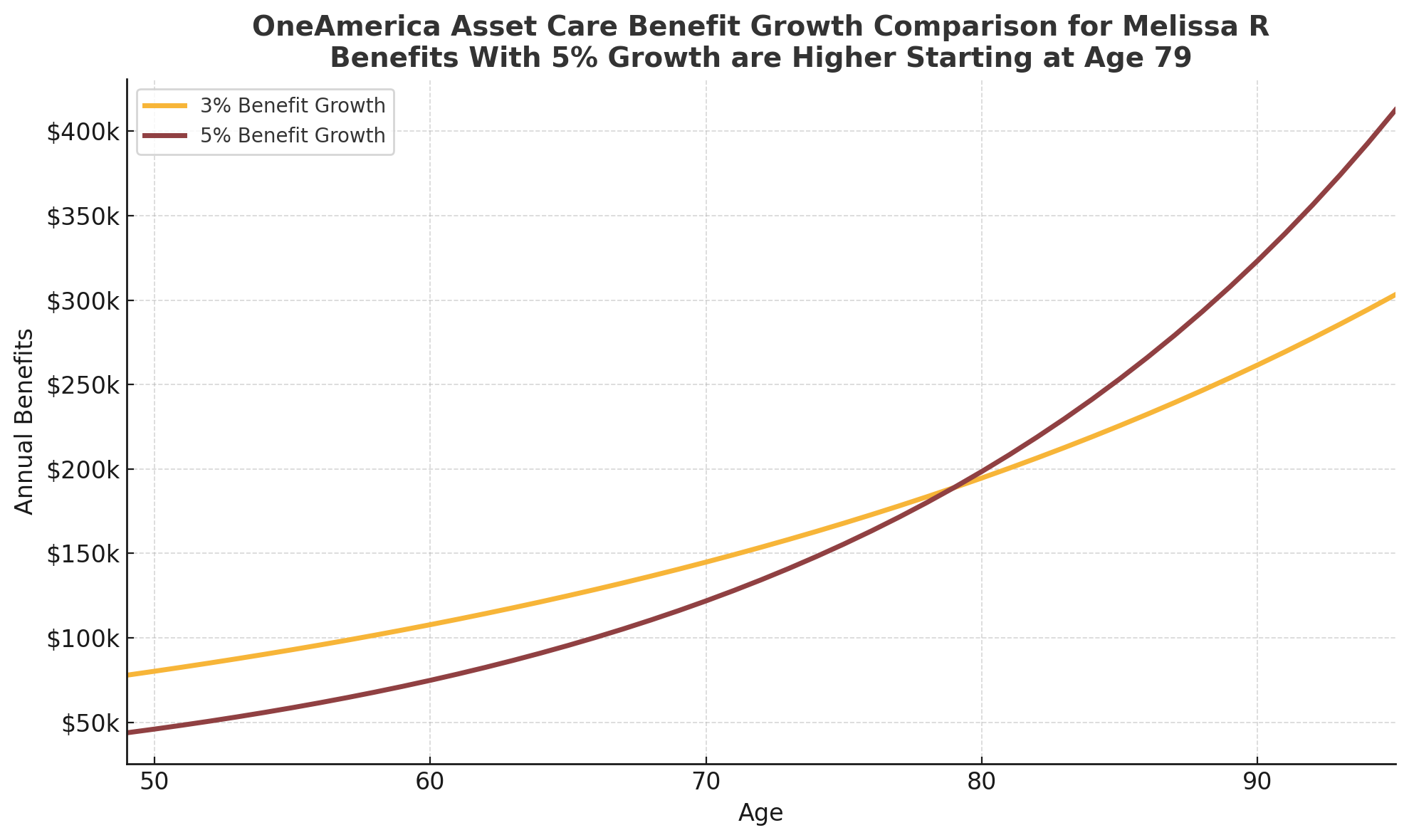

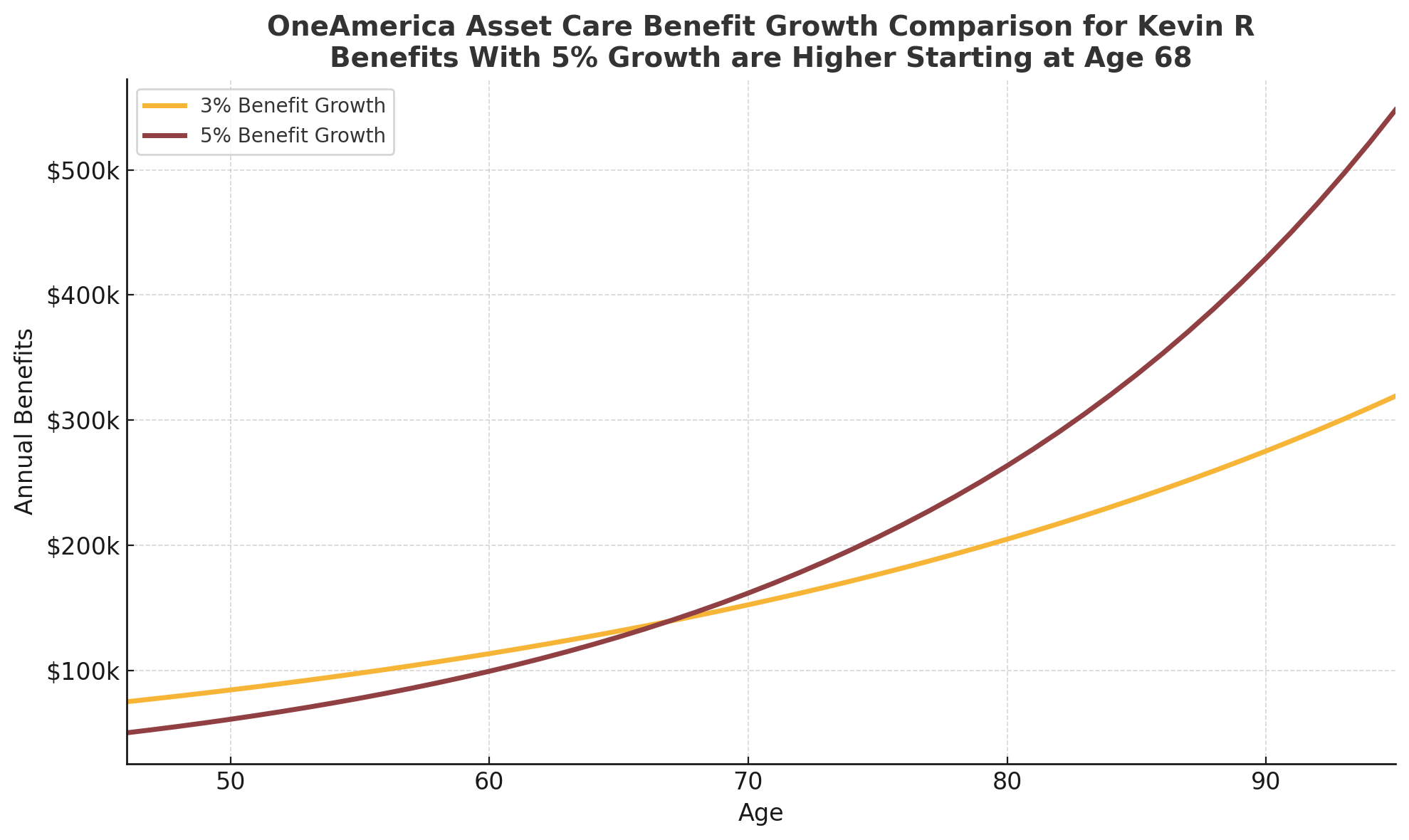

Let’s compare how annual benefits grow over time with OneAmerica’s Asset Care policy at 3% and 5%. Choosing 5% growth provides smaller benefits in the early years but larger benefits after about age 79 compared to the 3% option.

🧐 My thoughts: OneAmerica indicated that the Asset Care rating shown is a best-case scenario. Actual underwriting could result in a higher cost due to a less favorable rating.

For Annuity Care, OneAmerica indicated that lifetime benefits wouldn’t be offered, but an 8-year benefit duration should still be acceptable based on her health profile.

Given that, I’d recommend Melissa apply for Annuity Care (option C), which provides higher total potential benefits than Asset Care and avoids the risk of a formal decline appearing on future insurance applications. All quoted benefits are guaranteed, but the actual benefits could even be a little higher if non-guaranteed interest rates are credited.

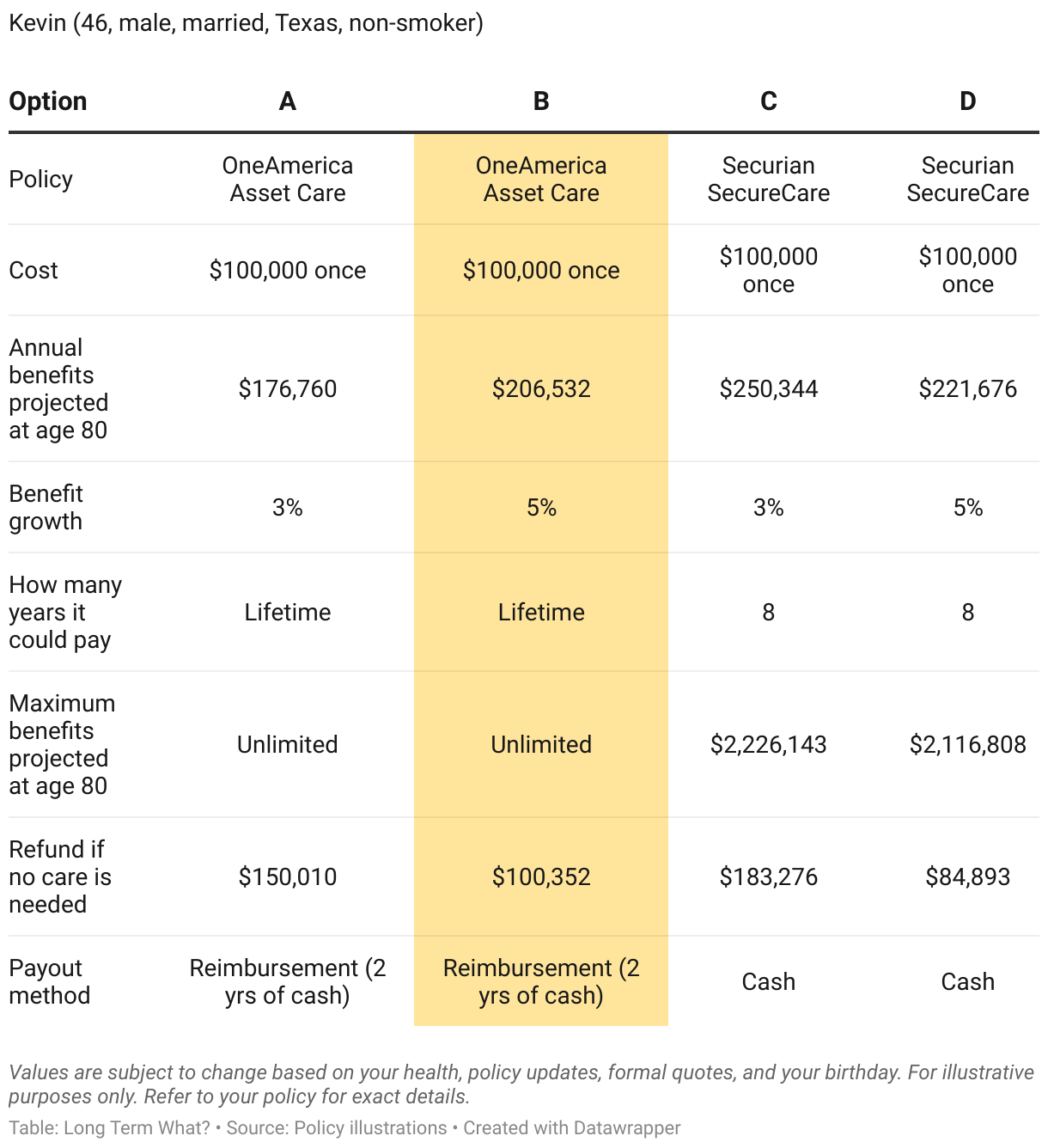

🔎 Kevin quotes

I selected policies with longer benefit periods to better address memory care risks, based on our earlier discussion. Each quote assumes a one-time $100,000 premium for easy comparison. These premiums can also be spread over five or ten years, which we can review later. The four quotes include two versions of the same policy with different benefit growth rates (3% and 5%).

When comparing the 5% growth option to the 3% growth option, OneAmerica reaches breakeven around age 68...

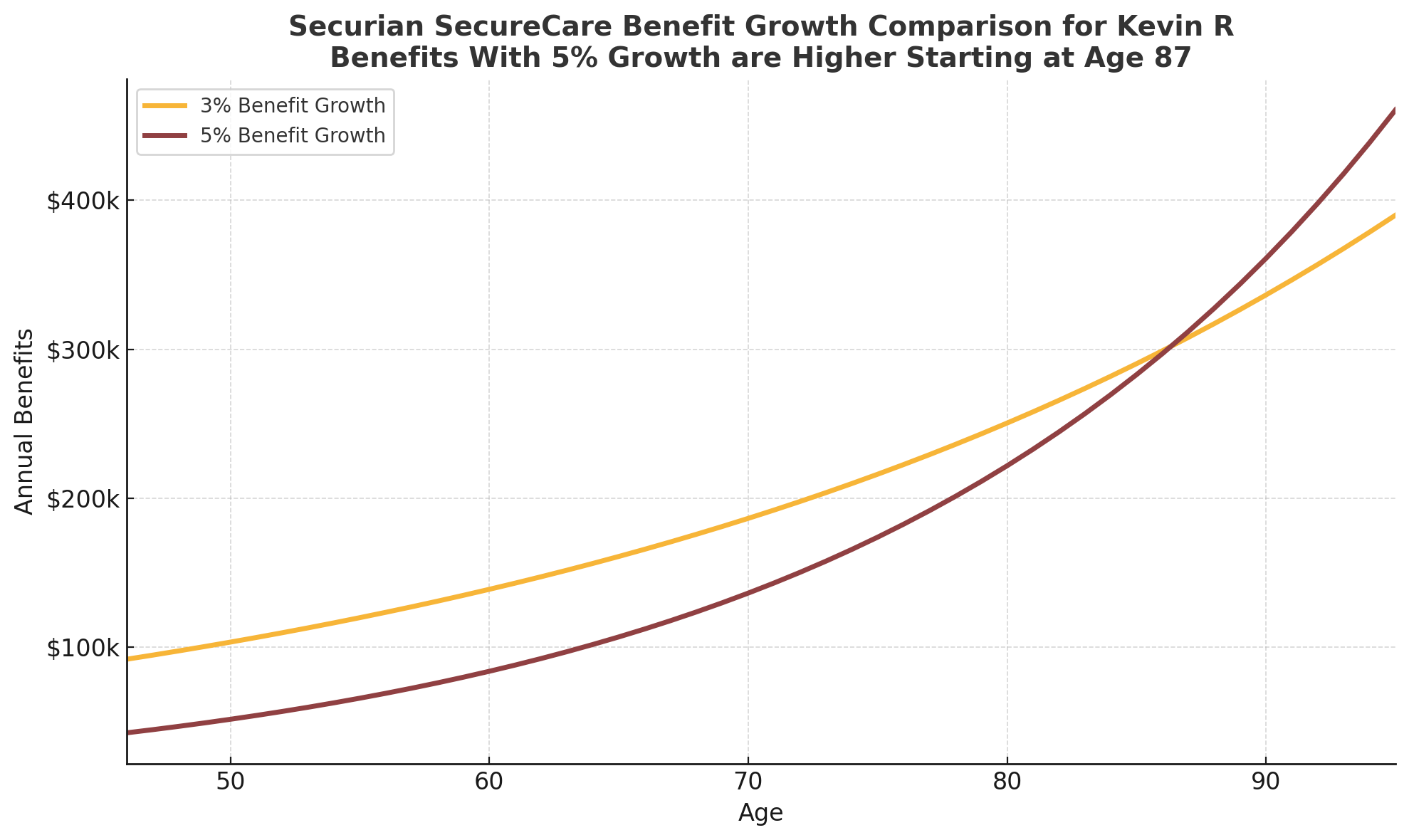

... while Securian’s breakeven is closer to age 87, meaning Securian charges relatively more for 5% growth.

🧐 My thoughts: I'd recommend option B, the OneAmerica Asset Care with 5% benefit growth for the lifetime benefits and more affordable 5% growth option.

For our call, I'll provide some feedback on the Northwest Mutual illustrations for comparison. Once we zero in on your preferences, I'll send over the policy illustrations which include various payment options.

Thanks,

Jesse

Jesse Vickey at Long Term What?

Schedule a call or 720-263-2188

Website | YouTube | Email