Emily,

Good news. Your revised long-term care (LTC) insurance quotes are ready for you and your financial advisor to review.

I included my step-by-step research notes below 🤓, but I tried to simplify it by providing you my top recommendations.

💰 How much insurance?

When we spoke, you said you wanted meaningful coverage—not to insure every dollar. The rest can be bridged with personal savings and Social Security.

By the time you turn 80 (around 2060), the average cost of assisted living in the U.S. is projected to be about $291,000 a year, assuming 4% annual growth. Costs vary a lot by region—DC, for example, is estimated at $427,000—but since it’s hard to know where you’ll be living 30+ years from now, we’ll use the national projection.

For meaningful coverage, I’ll target about 50%+ of the national projection, or roughly $140,000-$180,000 per year at age 80, in the quotes I share with you.

🛡️ What policy?

You mentioned wanting a policy that refunds your premiums if you never need care and pays benefits in cash rather than reimbursement. These are hybrid policies, and they come with other advantages too, including guaranteed premiums that never increase.

I reviewed the top hybrid options available. To keep the comparison consistent, the quotes below assume premiums of $7,500 per year (about $625 per month) for 10 years, with 4 years of benefits and 3% annual benefit growth.

My thoughts: Options B, C, and D offer the highest benefits. I’d lean toward option B (Nationwide) for a few reasons:

- The annual and maximum LTC benefits are very similar to C and D.

- Your heirs are guaranteed to receive a higher minimum refund than with the other options.

- Most policies don't start paying benefits until after a 90 day waiting period from when you first need care. The first 90 days of benefits are more certain than any other LTC payment. With Nationwide you’re paid for them in full on day 91.

- Nationwide offers the strongest benefits at 5% benefit growth (see below).

📈 5% benefit growth?

Since you’re under 45, it’s important to look closely at benefit growth options. All policies offer 3% and 5% growth, but Nationwide offers the best benefits if you choose 5%. At the same premium, switching to 5% gives you lower benefits in the near term but higher benefits later on when care is most often needed.

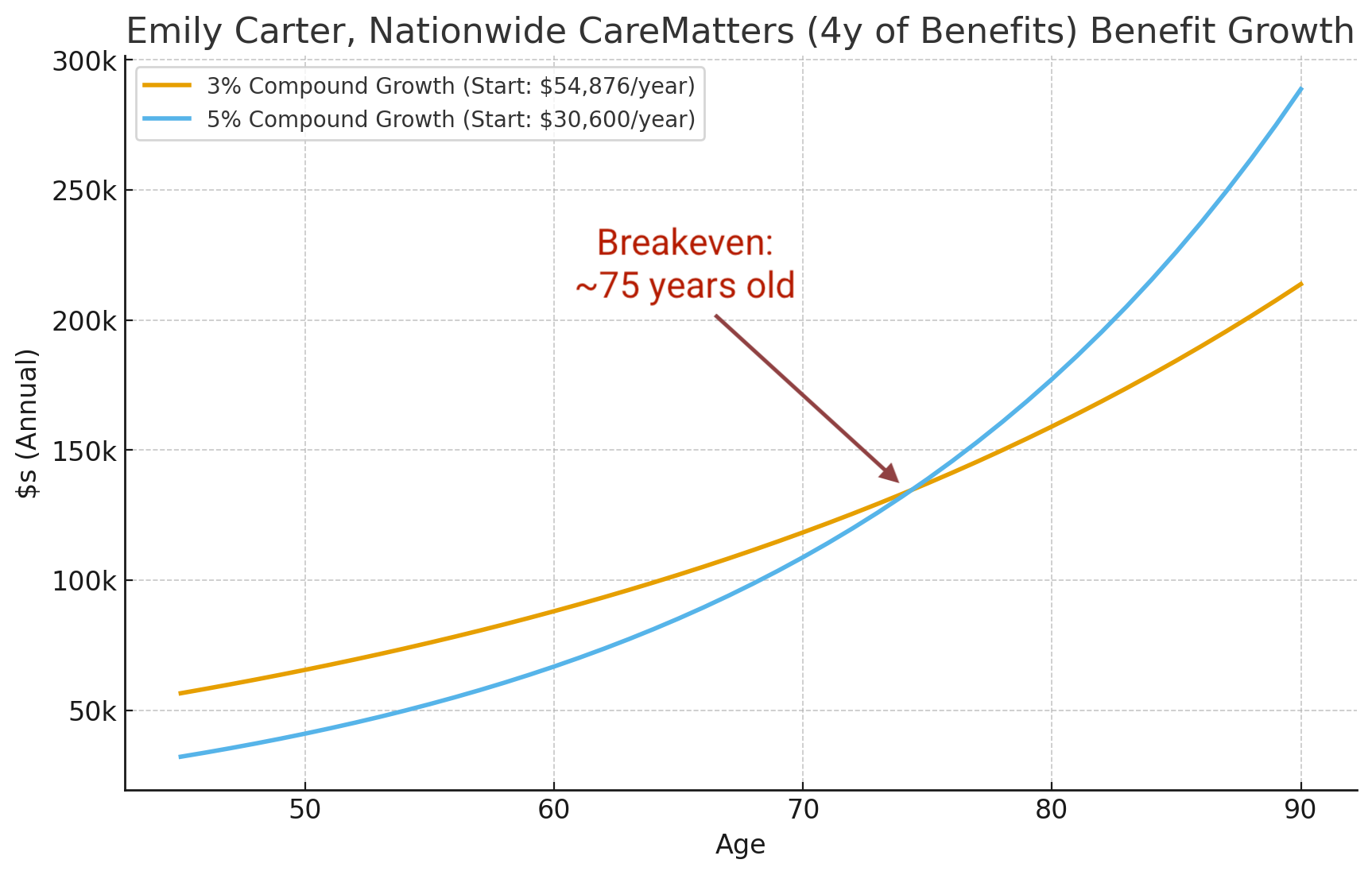

- For Nationwide CareMatters with 4 years of benefits, the 5% growth option surpasses the 3% option around age 75.

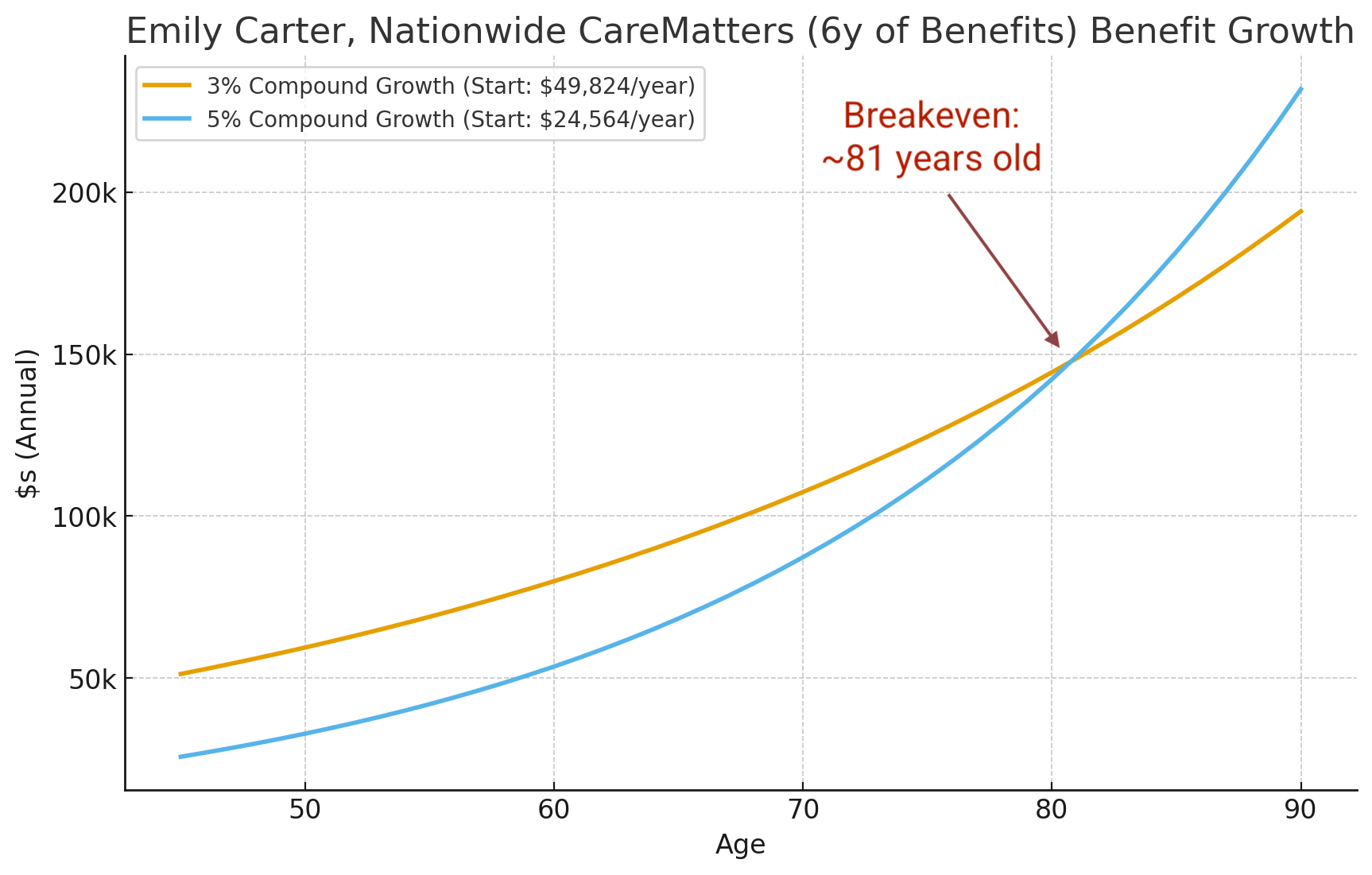

- For Nationwide CareMatters with 6 years of benefits, the 5% growth option surpasses the 3% option around age 81.

Based on these two graphs, the breakeven at age 75 (with 4 years of benefits) offers the strongest balance of breakeven and likelihood. The breakeven at age 81 (with 6 years of benefits) is reasonable, but in my view, it’s on the fence as a choice.

🔁 Revised quotes

Based on the research above, here are my three recommended options. Each is from Nationwide CareMatters, with the same premium of $7,500 per year (about $625 per month) for 10 years.

🧐 My suggestions

All three options are strong, and each includes a refund to your heirs if you never need care.

- Option 1: Best if you want the potentially highest total benefits.

- Option 2: Best if you want a solid balance of annual benefits and refund.

- Option 3: Best if you want the highest annual benefits, though with a lower refund.

Since the average length of care for women is 3.7 years—and annual costs can be higher than average depending on your state and type of care—I’d lean toward Option 3 with its four years of high annual benefits. That said, all three are excellent choices.

⬆️ ⬇️ If you'd like higher or lower annual benefits, you can adjust your premium and your benefits will rise proportionally (e.g., by 25%).

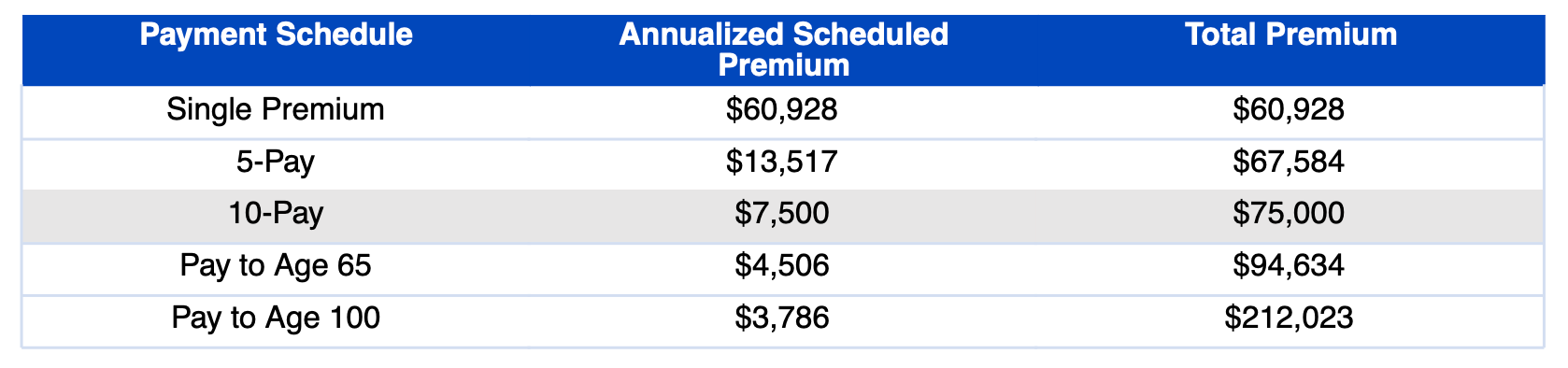

📆 Premium schedule

As we discussed on our call, these policies come with a few different payment schedules. I’ve outlined the options below (each option is similar). You also have the flexibility to pay monthly instead of annually.

👉🏻 Next steps

Once you've reviewed your options, just reply to my email or text with the one that feels closest—1, 2, or 3 and I'll email the policy documents to you (no commitment).

📺 Still learning?

Watch our 7-minute "unboring" video on the features of LTC insurance. That's me in the video.

Thanks,

Jesse

Jesse Vickey at Long Term What?

Schedule a call or 720-263-2188

Website | YouTube | Email